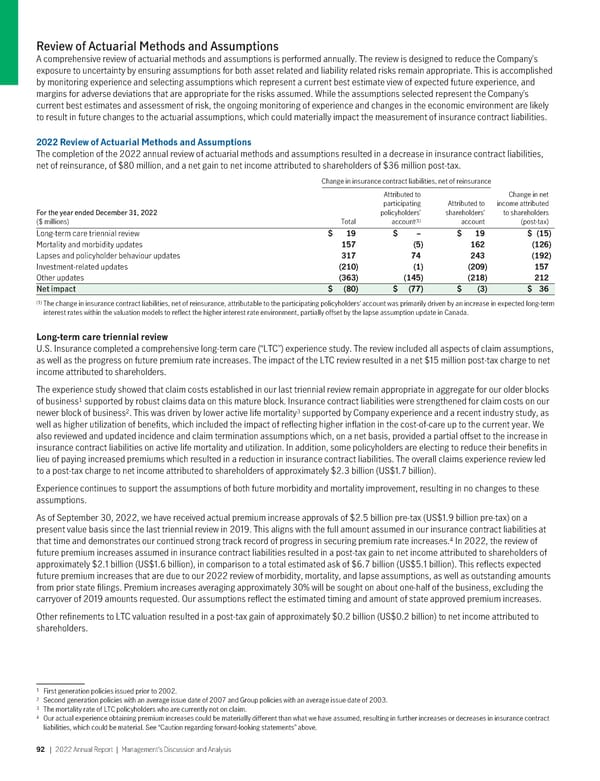

Review of Actuarial Methods and Assumptions A comprehensive review of actuarial methods and assumptions is performed annually. The review is designed to reduce the Company’s exposure to uncertainty by ensuring assumptions for both asset related and liability related risks remain appropriate. This is accomplished by monitoring experience and selecting assumptions which represent a current best estimate view of expected future experience, and margins for adverse deviations that are appropriate for the risks assumed. While the assumptions selected represent the Company’s current best estimates and assessment of risk, the ongoing monitoring of experience and changes in the economic environment are likely to result in future changes to the actuarial assumptions, which could materially impact the measurement of insurance contract liabilities. 2022ReviewofActuarialMethodsandAssumptions The completion of the 2022 annual review of actuarial methods and assumptions resulted in a decrease in insurance contract liabilities, net of reinsurance, of $80 million, and a net gain to net income attributed to shareholders of $36 million post-tax. Change in insurance contract liabilities, net of reinsurance Attributed to Change in net participating Attributed to income attributed For the year ended December 31, 2022 policyholders’ shareholders’ to shareholders ($ millions) Total (1) account account (post-tax) Long-term care triennial review $ 19 $ – $ 19 $ (15) Mortality and morbidity updates 157 (5) 162 (126) Lapses and policyholder behaviour updates 317 74 243 (192) Investment-related updates (210) (1) (209) 157 Other updates (363) (145) (218) 212 Net impact $ (80) $ (77) $ (3) $ 36 (1) The change in insurance contract liabilities, net of reinsurance, attributable to the participating policyholders’ account was primarily driven by an increase in expected long-term interest rates within the valuation models to reflect the higher interest rate environment, partially offset by the lapse assumption update in Canada. Long-termcaretriennialreview U.S. Insurance completed a comprehensive long-term care (“LTC”) experience study. The review included all aspects of claim assumptions, as well as the progress on future premium rate increases. The impact of the LTC review resulted in a net $15 million post-tax charge to net income attributed to shareholders. The experience study showed that claim costs established in our last triennial review remain appropriate in aggregate for our older blocks 1 supported by robust claims data on this mature block. Insurance contract liabilities were strengthened for claim costs on our of business 2 3 newer block of business . This was driven by lower active life mortality supported by Company experience and a recent industry study, as well as higher utilization of benefits, which included the impact of reflecting higher inflation in the cost-of-care up to the current year. We also reviewed and updated incidence and claim termination assumptions which, on a net basis, provided a partial offset to the increase in insurance contract liabilities on active life mortality and utilization. In addition, some policyholders are electing to reduce their benefits in lieu of paying increased premiums which resulted in a reduction in insurance contract liabilities. The overall claims experience review led to a post-tax charge to net income attributed to shareholders of approximately $2.3 billion (US$1.7 billion). Experience continues to support the assumptions of both future morbidity and mortality improvement, resulting in no changes to these assumptions. As of September 30, 2022, we have received actual premium increase approvals of $2.5 billion pre-tax (US$1.9 billion pre-tax) on a present value basis since the last triennial review in 2019. This aligns with the full amount assumed in our insurance contract liabilities at 4 In 2022, the review of that time and demonstrates our continued strong track record of progress in securing premium rate increases. future premium increases assumed in insurance contract liabilities resulted in a post-tax gain to net income attributed to shareholders of approximately $2.1 billion (US$1.6 billion), in comparison to a total estimated ask of $6.7 billion (US$5.1 billion). This reflects expected future premium increases that are due to our 2022 review of morbidity, mortality, and lapse assumptions, as well as outstanding amounts from prior state filings. Premium increases averaging approximately 30% will be sought on about one-half of the business, excluding the carryover of 2019 amounts requested. Our assumptions reflect the estimated timing and amount of state approved premium increases. Other refinements to LTC valuation resulted in a post-tax gain of approximately $0.2 billion (US$0.2 billion) to net income attributed to shareholders. 1 First generation policies issued prior to 2002. 2 Second generation policies with an average issue date of 2007 and Group policies with an average issue date of 2003. 3 The mortality rate of LTC policyholders who are currently not on claim. 4 Our actual experience obtaining premium increases could be materially different than what we have assumed, resulting in further increases or decreases in insurance contract liabilities, which could be material. See “Caution regarding forward-looking statements” above. 92 | 2022AnnualReport | Management’sDiscussionandAnalysis

2022 Annual Report Page 93 Page 95

2022 Annual Report Page 93 Page 95