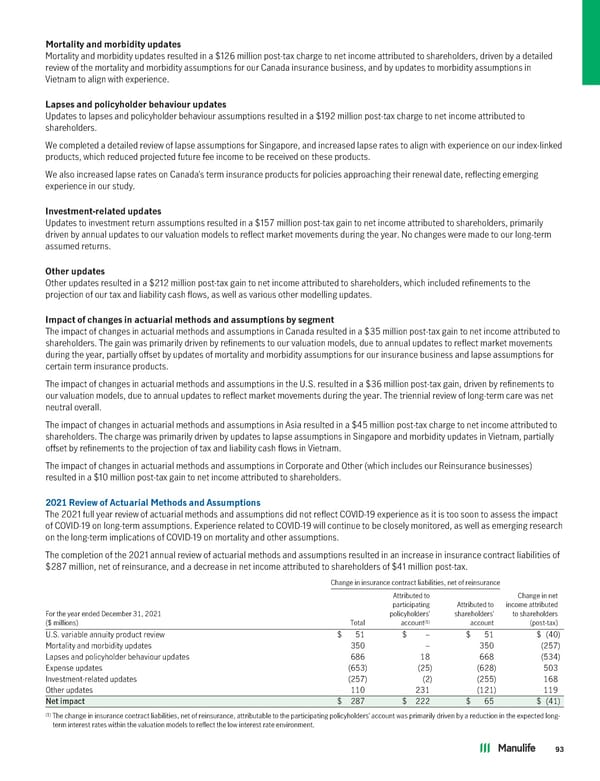

Mortalityandmorbidityupdates Mortality and morbidity updates resulted in a $126 million post-tax charge to net income attributed to shareholders, driven by a detailed review of the mortality and morbidity assumptions for our Canada insurance business, and by updates to morbidity assumptions in Vietnam to align with experience. Lapsesandpolicyholderbehaviourupdates Updates to lapses and policyholder behaviour assumptions resulted in a $192 million post-tax charge to net income attributed to shareholders. We completed a detailed review of lapse assumptions for Singapore, and increased lapse rates to align with experience on our index-linked products, which reduced projected future fee income to be received on these products. We also increased lapse rates on Canada’s term insurance products for policies approaching their renewal date, reflecting emerging experience in our study. Investment-relatedupdates Updates to investment return assumptions resulted in a $157 million post-tax gain to net income attributed to shareholders, primarily driven by annual updates to our valuation models to reflect market movements during the year. No changes were made to our long-term assumed returns. Otherupdates Other updates resulted in a $212 million post-tax gain to net income attributed to shareholders, which included refinements to the projection of our tax and liability cash flows, as well as various other modelling updates. Impactofchangesinactuarialmethodsandassumptionsbysegment The impact of changes in actuarial methods and assumptions in Canada resulted in a $35 million post-tax gain to net income attributed to shareholders. The gain was primarily driven by refinements to our valuation models, due to annual updates to reflect market movements during the year, partially offset by updates of mortality and morbidity assumptions for our insurance business and lapse assumptions for certain term insurance products. The impact of changes in actuarial methods and assumptions in the U.S. resulted in a $36 million post-tax gain, driven by refinements to our valuation models, due to annual updates to reflect market movements during the year. The triennial review of long-term care was net neutral overall. The impact of changes in actuarial methods and assumptions in Asia resulted in a $45 million post-tax charge to net income attributed to shareholders. The charge was primarily driven by updates to lapse assumptions in Singapore and morbidity updates in Vietnam, partially offset by refinements to the projection of tax and liability cash flows in Vietnam. The impact of changes in actuarial methods and assumptions in Corporate and Other (which includes our Reinsurance businesses) resulted in a $10 million post-tax gain to net income attributed to shareholders. 2021ReviewofActuarialMethodsandAssumptions The 2021 full year review of actuarial methods and assumptions did not reflect COVID-19 experience as it is too soon to assess the impact of COVID-19 on long-term assumptions. Experience related to COVID-19 will continue to be closely monitored, as well as emerging research on the long-term implications of COVID-19 on mortality and other assumptions. The completion of the 2021 annual review of actuarial methods and assumptions resulted in an increase in insurance contract liabilities of $287 million, net of reinsurance, and a decrease in net income attributed to shareholders of $41 million post-tax. Change in insurance contract liabilities, net of reinsurance Attributed to Change in net participating Attributed to income attributed For the year ended December 31, 2021 policyholders’ shareholders’ to shareholders ($ millions) Total (1) account account (post-tax) U.S. variable annuity product review $ 51 $ – $ 51 $ (40) Mortality and morbidity updates 350 – 350 (257) Lapses and policyholder behaviour updates 686 18 668 (534) Expense updates (653) (25) (628) 503 Investment-related updates (257) (2) (255) 168 Other updates 110 231 (121) 119 Net impact $ 287 $ 222 $ 65 $ (41) (1) The change in insurance contract liabilities, net of reinsurance, attributable to the participating policyholders’ account was primarily driven by a reduction in the expected long- term interest rates within the valuation models to reflect the low interest rate environment. 93

2022 Annual Report Page 94 Page 96

2022 Annual Report Page 94 Page 96