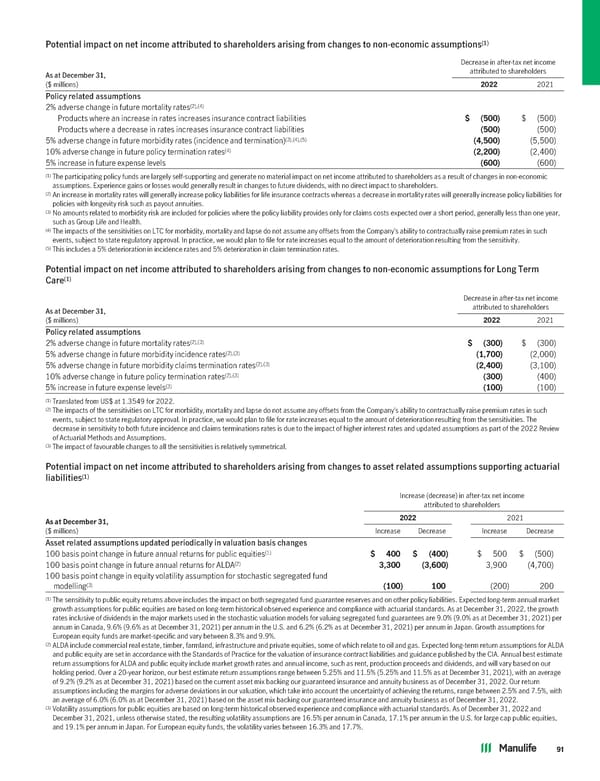

(1) Potential impact on net income attributed to shareholders arising from changes to non-economic assumptions Decrease in after-tax net income As at December 31, attributed to shareholders ($ millions) 2022 2021 Policy related assumptions (2),(4) 2% adverse change in future mortality rates Products where an increase in rates increases insurance contract liabilities $ (500) $ (500) Products where a decrease in rates increases insurance contract liabilities (500) (500) (3),(4),(5) 5% adverse change in future morbidity rates (incidence and termination) (4,500) (5,500) (4) 10% adverse change in future policy termination rates (2,200) (2,400) 5% increase in future expense levels (600) (600) (1) The participating policy funds are largely self-supporting and generate no material impact on net income attributed to shareholders as a result of changes in non-economic assumptions. Experience gains or losses would generally result in changes to future dividends, with no direct impact to shareholders. (2) An increase in mortality rates will generally increase policy liabilities for life insurance contracts whereas a decrease in mortality rates will generally increase policy liabilities for policies with longevity risk such as payout annuities. (3) No amounts related to morbidity risk are included for policies where the policy liability provides only for claims costs expected over a short period, generally less than one year, such as Group Life and Health. (4) The impacts of the sensitivities on LTC for morbidity, mortality and lapse do not assume any offsets from the Company’s ability to contractually raise premium rates in such events, subject to state regulatory approval. In practice, we would plan to file for rate increases equal to the amount of deterioration resulting from the sensitivity. (5) This includes a 5% deterioration in incidence rates and 5% deterioration in claim termination rates. Potential impact on net income attributed to shareholders arising from changes to non-economic assumptions for Long Term (1) Care Decrease in after-tax net income As at December 31, attributed to shareholders ($ millions) 2022 2021 Policy related assumptions (2),(3) 2% adverse change in future mortality rates $ (300) $ (300) (2),(3) 5% adverse change in future morbidity incidence rates (1,700) (2,000) (2),(3) 5% adverse change in future morbidity claims termination rates (2,400) (3,100) (2),(3) 10% adverse change in future policy termination rates (300) (400) (3) 5% increase in future expense levels (100) (100) (1) Translated from US$ at 1.3549 for 2022. (2) The impacts of the sensitivities on LTC for morbidity, mortality and lapse do not assume any offsets from the Company’s ability to contractually raise premium rates in such events, subject to state regulatory approval. In practice, we would plan to file for rate increases equal to the amount of deterioration resulting from the sensitivities. The decrease in sensitivity to both future incidence and claims terminations rates is due to the impact of higher interest rates and updated assumptions as part of the 2022 Review of Actuarial Methods and Assumptions. (3) The impact of favourable changes to all the sensitivities is relatively symmetrical. Potential impact on net income attributed to shareholders arising from changes to asset related assumptions supporting actuarial (1) liabilities Increase (decrease) in after-tax net income attributed to shareholders AsatDecember31, 2022 2021 ($ millions) Increase Decrease Increase Decrease Asset related assumptions updated periodically in valuation basis changes (1) 100 basis point change in future annual returns for public equities $ 400 $ (400) $ 500 $ (500) (2) 100 basis point change in future annual returns for ALDA 3,300 (3,600) 3,900 (4,700) 100 basis point change in equity volatility assumption for stochastic segregated fund (3) modelling (100) 100 (200) 200 (1) The sensitivity to public equity returns above includes the impact on both segregated fund guarantee reserves and on other policy liabilities. Expected long-term annual market growth assumptions for public equities are based on long-term historical observed experience and compliance with actuarial standards. As at December 31, 2022, the growth rates inclusive of dividends in the major markets used in the stochastic valuation models for valuing segregated fund guarantees are 9.0% (9.0% as at December 31, 2021) per annum in Canada, 9.6% (9.6% as at December 31, 2021) per annum in the U.S. and 6.2% (6.2% as at December 31, 2021) per annum in Japan. Growth assumptions for European equity funds are market-specific and vary between 8.3% and 9.9%. (2) ALDA include commercial real estate, timber, farmland, infrastructure and private equities, some of which relate to oil and gas. Expected long-term return assumptions for ALDA and public equity are set in accordance with the Standards of Practice for the valuation of insurance contract liabilities and guidance published by the CIA. Annual best estimate return assumptions for ALDA and public equity include market growth rates and annual income, such as rent, production proceeds and dividends, and will vary based on our holding period. Over a 20-year horizon, our best estimate return assumptions range between 5.25% and 11.5% (5.25% and 11.5% as at December 31, 2021), with an average of 9.2% (9.2% as at December 31, 2021) based on the current asset mix backing our guaranteed insurance and annuity business as of December 31, 2022. Our return assumptions including the margins for adverse deviations in our valuation, which take into account the uncertainty of achieving the returns, range between 2.5% and 7.5%, with an average of 6.0% (6.0% as at December 31, 2021) based on the asset mix backing our guaranteed insurance and annuity business as of December 31, 2022. (3) Volatility assumptions for public equities are based on long-term historical observed experience and compliance with actuarial standards. As of December 31, 2022 and December 31, 2021, unless otherwise stated, the resulting volatility assumptions are 16.5% per annum in Canada, 17.1% per annum in the U.S. for large cap public equities, and 19.1% per annum in Japan. For European equity funds, the volatility varies between 16.3% and 17.7%. 91

2022 Annual Report Page 92 Page 94

2022 Annual Report Page 92 Page 94