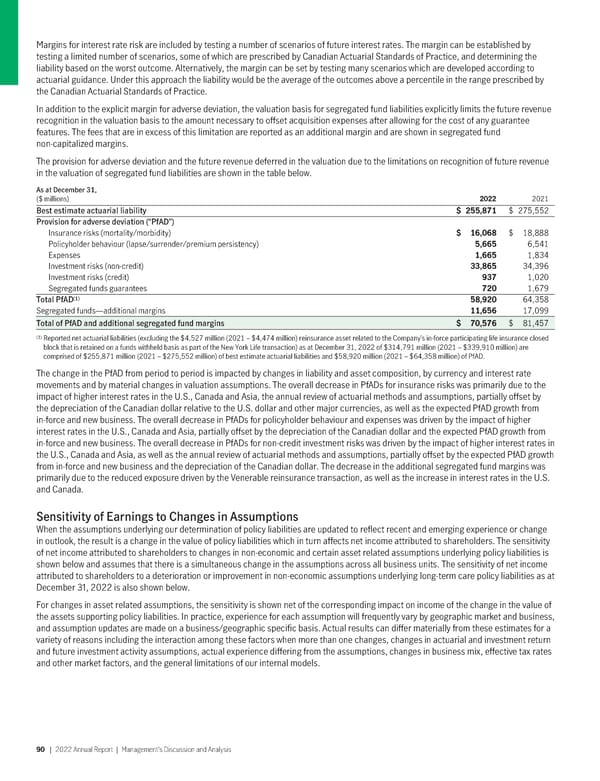

Margins for interest rate risk are included by testing a number of scenarios of future interest rates. The margin can be established by testing a limited number of scenarios, some of which are prescribed by Canadian Actuarial Standards of Practice, and determining the liability based on the worst outcome. Alternatively, the margin can be set by testing many scenarios which are developed according to actuarial guidance. Under this approach the liability would be the average of the outcomes above a percentile in the range prescribed by the Canadian Actuarial Standards of Practice. In addition to the explicit margin for adverse deviation, the valuation basis for segregated fund liabilities explicitly limits the future revenue recognition in the valuation basis to the amount necessary to offset acquisition expenses after allowing for the cost of any guarantee features. The fees that are in excess of this limitation are reported as an additional margin and are shown in segregated fund non-capitalized margins. The provision for adverse deviation and the future revenue deferred in the valuation due to the limitations on recognition of future revenue in the valuation of segregated fund liabilities are shown in the table below. As at December 31, ($ millions) 2022 2021 Best estimate actuarial liability $ 255,871 $ 275,552 Provision for adverse deviation (“PfAD”) Insurance risks (mortality/morbidity) $ 16,068 $ 18,888 Policyholder behaviour (lapse/surrender/premium persistency) 5,665 6,541 Expenses 1,665 1,834 Investment risks (non-credit) 33,865 34,396 Investment risks (credit) 937 1,020 Segregated funds guarantees 720 1,679 (1) Total PfAD 58,920 64,358 Segregated funds—additional margins 11,656 17,099 Total of PfAD and additional segregated fund margins $ 70,576 $ 81,457 (1) Reported net actuarial liabilities (excluding the $4,527 million (2021 – $4,474 million) reinsurance asset related to the Company’s in-force participating life insurance closed block that is retained on a funds withheld basis as part of the New York Life transaction) as at December 31, 2022 of $314,791 million (2021 – $339,910 million) are comprised of $255,871 million (2021 – $275,552 million) of best estimate actuarial liabilities and $58,920 million (2021 – $64,358 million) of PfAD. The change in the PfAD from period to period is impacted by changes in liability and asset composition, by currency and interest rate movements and by material changes in valuation assumptions. The overall decrease in PfADs for insurance risks was primarily due to the impact of higher interest rates in the U.S., Canada and Asia, the annual review of actuarial methods and assumptions, partially offset by the depreciation of the Canadian dollar relative to the U.S. dollar and other major currencies, as well as the expected PfAD growth from in-force and new business. The overall decrease in PfADs for policyholder behaviour and expenses was driven by the impact of higher interest rates in the U.S., Canada and Asia, partially offset by the depreciation of the Canadian dollar and the expected PfAD growth from in-force and new business. The overall decrease in PfADs for non-credit investment risks was driven by the impact of higher interest rates in the U.S., Canada and Asia, as well as the annual review of actuarial methods and assumptions, partially offset by the expected PfAD growth from in-force and new business and the depreciation of the Canadian dollar. The decrease in the additional segregated fund margins was primarily due to the reduced exposure driven by the Venerable reinsurance transaction, as well as the increase in interest rates in the U.S. and Canada. Sensitivity of Earnings to Changes in Assumptions When the assumptions underlying our determination of policy liabilities are updated to reflect recent and emerging experience or change in outlook, the result is a change in the value of policy liabilities which in turn affects net income attributed to shareholders. The sensitivity of net income attributed to shareholders to changes in non-economic and certain asset related assumptions underlying policy liabilities is shown below and assumes that there is a simultaneous change in the assumptions across all business units. The sensitivity of net income attributed to shareholders to a deterioration or improvement in non-economic assumptions underlying long-term care policy liabilities as at December 31, 2022 is also shown below. For changes in asset related assumptions, the sensitivity is shown net of the corresponding impact on income of the change in the value of the assets supporting policy liabilities. In practice, experience for each assumption will frequently vary by geographic market and business, and assumption updates are made on a business/geographic specific basis. Actual results can differ materially from these estimates for a variety of reasons including the interaction among these factors when more than one changes, changes in actuarial and investment return and future investment activity assumptions, actual experience differing from the assumptions, changes in business mix, effective tax rates and other market factors, and the general limitations of our internal models. 90 | 2022AnnualReport | Management’sDiscussionandAnalysis

2022 Annual Report Page 91 Page 93

2022 Annual Report Page 91 Page 93