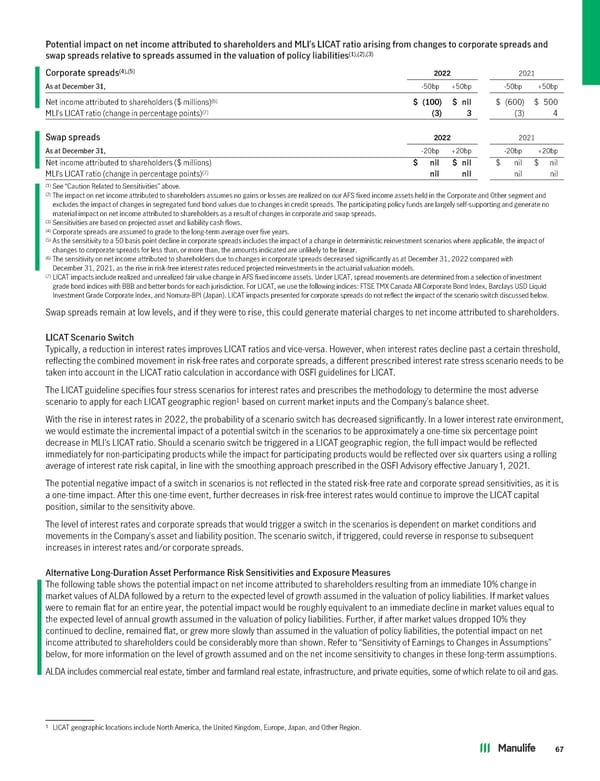

Potential impact on net income attributed to shareholders and MLI’s LICAT ratio arising from changes to corporate spreads and (1),(2),(3) swap spreads relative to spreads assumed in the valuation of policy liabilities (4),(5) Corporate spreads 2022 2021 As at December 31, -50bp +50bp -50bp +50bp (6) Net income attributed to shareholders ($ millions) $ (100) $ nil $ (600) $ 500 (7) MLI’s LICAT ratio (change in percentage points) (3) 3 (3) 4 Swap spreads 2022 2021 As at December 31, -20bp +20bp -20bp +20bp Net income attributed to shareholders ($ millions) $ nil $ nil $ nil $ nil (7) MLI’s LICAT ratio (change in percentage points) nil nil nil nil (1) See “Caution Related to Sensitivities” above. (2) The impact on net income attributed to shareholders assumes no gains or losses are realized on our AFS fixed income assets held in the Corporate and Other segment and excludes the impact of changes in segregated fund bond values due to changes in credit spreads. The participating policy funds are largely self-supporting and generate no material impact on net income attributed to shareholders as a result of changes in corporate and swap spreads. (3) Sensitivities are based on projected asset and liability cash flows. (4) Corporate spreads are assumed to grade to the long-term average over five years. (5) As the sensitivity to a 50 basis point decline in corporate spreads includes the impact of a change in deterministic reinvestment scenarios where applicable, the impact of changes to corporate spreads for less than, or more than, the amounts indicated are unlikely to be linear. (6) The sensitivity on net income attributed to shareholders due to changes in corporate spreads decreased significantly as at December 31, 2022 compared with December 31, 2021, as the rise in risk-free interest rates reduced projected reinvestments in the actuarial valuation models. (7) LICAT impacts include realized and unrealized fair value change in AFS fixed income assets. Under LICAT, spread movements are determined from a selection of investment grade bond indices with BBB and better bonds for each jurisdiction. For LICAT, we use the following indices: FTSE TMX Canada All Corporate Bond Index, Barclays USD Liquid Investment Grade Corporate Index, and Nomura-BPI (Japan). LICAT impacts presented for corporate spreads do not reflect the impact of the scenario switch discussed below. Swap spreads remain at low levels, and if they were to rise, this could generate material charges to net income attributed to shareholders. LICAT Scenario Switch Typically, a reduction in interest rates improves LICAT ratios and vice-versa. However, when interest rates decline past a certain threshold, reflecting the combined movement in risk-free rates and corporate spreads, a different prescribed interest rate stress scenario needs to be taken into account in the LICAT ratio calculation in accordance with OSFI guidelines for LICAT. The LICAT guideline specifies four stress scenarios for interest rates and prescribes the methodology to determine the most adverse 1 based on current market inputs and the Company’s balance sheet. scenario to apply for each LICAT geographic region With the rise in interest rates in 2022, the probability of a scenario switch has decreased significantly. In a lower interest rate environment, we would estimate the incremental impact of a potential switch in the scenarios to be approximately a one-time six percentage point decrease in MLI’s LICAT ratio. Should a scenario switch be triggered in a LICAT geographic region, the full impact would be reflected immediately for non-participating products while the impact for participating products would be reflected over six quarters using a rolling average of interest rate risk capital, in line with the smoothing approach prescribed in the OSFI Advisory effective January 1, 2021. The potential negative impact of a switch in scenarios is not reflected in the stated risk-free rate and corporate spread sensitivities, as it is a one-time impact. After this one-time event, further decreases in risk-free interest rates would continue to improve the LICAT capital position, similar to the sensitivity above. The level of interest rates and corporate spreads that would trigger a switch in the scenarios is dependent on market conditions and movements in the Company’s asset and liability position. The scenario switch, if triggered, could reverse in response to subsequent increases in interest rates and/or corporate spreads. Alternative Long-Duration Asset Performance Risk Sensitivities and Exposure Measures The following table shows the potential impact on net income attributed to shareholders resulting from an immediate 10% change in market values of ALDA followed by a return to the expected level of growth assumed in the valuation of policy liabilities. If market values were to remain flat for an entire year, the potential impact would be roughly equivalent to an immediate decline in market values equal to the expected level of annual growth assumed in the valuation of policy liabilities. Further, if after market values dropped 10% they continued to decline, remained flat, or grew more slowly than assumed in the valuation of policy liabilities, the potential impact on net income attributed to shareholders could be considerably more than shown. Refer to “Sensitivity of Earnings to Changes in Assumptions” below, for more information on the level of growth assumed and on the net income sensitivity to changes in these long-term assumptions. ALDA includes commercial real estate, timber and farmland real estate, infrastructure, and private equities, some of which relate to oil and gas. 1 LICAT geographic locations include North America, the United Kingdom, Europe, Japan, and Other Region. 67

2022 Annual Report Page 68 Page 70

2022 Annual Report Page 68 Page 70