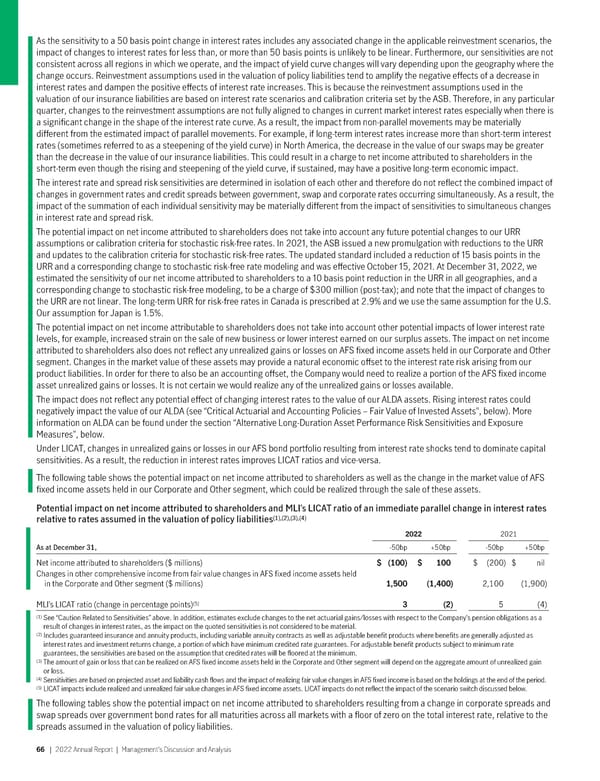

As the sensitivity to a 50 basis point change in interest rates includes any associated change in the applicable reinvestment scenarios, the impact of changes to interest rates for less than, or more than 50 basis points is unlikely to be linear. Furthermore, our sensitivities are not consistent across all regions in which we operate, and the impact of yield curve changes will vary depending upon the geography where the change occurs. Reinvestment assumptions used in the valuation of policy liabilities tend to amplify the negative effects of a decrease in interest rates and dampen the positive effects of interest rate increases. This is because the reinvestment assumptions used in the valuation of our insurance liabilities are based on interest rate scenarios and calibration criteria set by the ASB. Therefore, in any particular quarter, changes to the reinvestment assumptions are not fully aligned to changes in current market interest rates especially when there is a significant change in the shape of the interest rate curve. As a result, the impact from non-parallel movements may be materially different from the estimated impact of parallel movements. For example, if long-term interest rates increase more than short-term interest rates (sometimes referred to as a steepening of the yield curve) in North America, the decrease in the value of our swaps may be greater than the decrease in the value of our insurance liabilities. This could result in a charge to net income attributed to shareholders in the short-term even though the rising and steepening of the yield curve, if sustained, may have a positive long-term economic impact. The interest rate and spread risk sensitivities are determined in isolation of each other and therefore do not reflect the combined impact of changes in government rates and credit spreads between government, swap and corporate rates occurring simultaneously. As a result, the impact of the summation of each individual sensitivity may be materially different from the impact of sensitivities to simultaneous changes in interest rate and spread risk. The potential impact on net income attributed to shareholders does not take into account any future potential changes to our URR assumptions or calibration criteria for stochastic risk-free rates. In 2021, the ASB issued a new promulgation with reductions to the URR and updates to the calibration criteria for stochastic risk-free rates. The updated standard included a reduction of 15 basis points in the URR and a corresponding change to stochastic risk-free rate modeling and was effective October 15, 2021. At December 31, 2022, we estimated the sensitivity of our net income attributed to shareholders to a 10 basis point reduction in the URR in all geographies, and a corresponding change to stochastic risk-free modeling, to be a charge of $300 million (post-tax); and note that the impact of changes to the URR are not linear. The long-term URR for risk-free rates in Canada is prescribed at 2.9% and we use the same assumption for the U.S. Our assumption for Japan is 1.5%. The potential impact on net income attributable to shareholders does not take into account other potential impacts of lower interest rate levels, for example, increased strain on the sale of new business or lower interest earned on our surplus assets. The impact on net income attributed to shareholders also does not reflect any unrealized gains or losses on AFS fixed income assets held in our Corporate and Other segment. Changes in the market value of these assets may provide a natural economic offset to the interest rate risk arising from our product liabilities. In order for there to also be an accounting offset, the Company would need to realize a portion of the AFS fixed income asset unrealized gains or losses. It is not certain we would realize any of the unrealized gains or losses available. The impact does not reflect any potential effect of changing interest rates to the value of our ALDA assets. Rising interest rates could negatively impact the value of our ALDA (see “Critical Actuarial and Accounting Policies – Fair Value of Invested Assets”, below). More information on ALDA can be found under the section “Alternative Long-Duration Asset Performance Risk Sensitivities and Exposure Measures”, below. Under LICAT, changes in unrealized gains or losses in our AFS bond portfolio resulting from interest rate shocks tend to dominate capital sensitivities. As a result, the reduction in interest rates improves LICAT ratios and vice-versa. The following table shows the potential impact on net income attributed to shareholders as well as the change in the market value of AFS fixed income assets held in our Corporate and Other segment, which could be realized through the sale of these assets. Potential impact on net income attributed to shareholders and MLI’s LICAT ratio of an immediate parallel change in interest rates (1),(2),(3),(4) relative to rates assumed in the valuation of policy liabilities 2022 2021 As at December 31, -50bp +50bp -50bp +50bp Net income attributed to shareholders ($ millions) $ (100) $ 100 $ (200) $ nil Changes in other comprehensive income from fair value changes in AFS fixed income assets held in the Corporate and Other segment ($ millions) 1,500 (1,400) 2,100 (1,900) (5) MLI’s LICAT ratio (change in percentage points) 3(2)5 (4) (1) See “Caution Related to Sensitivities” above. In addition, estimates exclude changes to the net actuarial gains/losses with respect to the Company’s pension obligations as a result of changes in interest rates, as the impact on the quoted sensitivities is not considered to be material. (2) Includes guaranteed insurance and annuity products, including variable annuity contracts as well as adjustable benefit products where benefits are generally adjusted as interest rates and investment returns change, a portion of which have minimum credited rate guarantees. For adjustable benefit products subject to minimum rate guarantees, the sensitivities are based on the assumption that credited rates will be floored at the minimum. (3) The amount of gain or loss that can be realized on AFS fixed income assets held in the Corporate and Other segment will depend on the aggregate amount of unrealized gain or loss. (4) Sensitivities are based on projected asset and liability cash flows and the impact of realizing fair value changes in AFS fixed income is based on the holdings at the end of the period. (5) LICAT impacts include realized and unrealized fair value changes in AFS fixed income assets. LICAT impacts do not reflect the impact of the scenario switch discussed below. The following tables show the potential impact on net income attributed to shareholders resulting from a change in corporate spreads and swap spreads over government bond rates for all maturities across all markets with a floor of zero on the total interest rate, relative to the spreads assumed in the valuation of policy liabilities. 66 | 2022AnnualReport | Management’sDiscussionandAnalysis

2022 Annual Report Page 67 Page 69

2022 Annual Report Page 67 Page 69