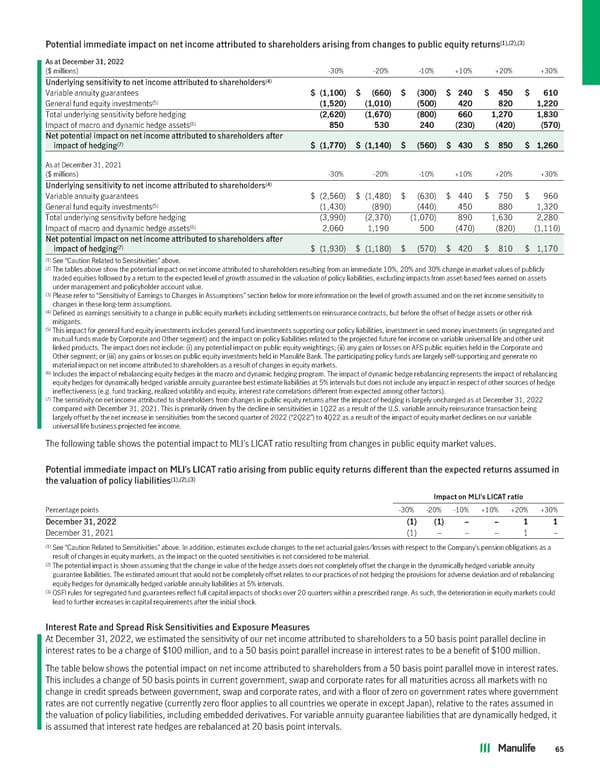

(1),(2),(3) Potential immediate impact on net income attributed to shareholders arising from changes to public equity returns As at December 31, 2022 ($ millions) -30% -20% -10% +10% +20% +30% (4) Underlying sensitivity to net income attributed to shareholders Variable annuity guarantees $ (1,100) $ (660) $ (300) $ 240 $ 450 $ 610 (5) General fund equity investments (1,520) (1,010) (500) 420 820 1,220 Total underlying sensitivity before hedging (2,620) (1,670) (800) 660 1,270 1,830 (6) Impact of macro and dynamic hedge assets 850 530 240 (230) (420) (570) Net potential impact on net income attributed to shareholders after (7) impact of hedging $ (1,770) $ (1,140) $ (560) $ 430 $ 850 $ 1,260 As at December 31, 2021 ($ millions) -30% -20% -10% +10% +20% +30% (4) Underlying sensitivity to net income attributed to shareholders Variable annuity guarantees $ (2,560) $ (1,480) $ (630) $ 440 $ 750 $ 960 (5) General fund equity investments (1,430) (890) (440) 450 880 1,320 Total underlying sensitivity before hedging (3,990) (2,370) (1,070) 890 1,630 2,280 (6) Impact of macro and dynamic hedge assets 2,060 1,190 500 (470) (820) (1,110) Net potential impact on net income attributed to shareholders after (7) impact of hedging $ (1,930) $ (1,180) $ (570) $ 420 $ 810 $ 1,170 (1) See “Caution Related to Sensitivities” above. (2) The tables above show the potential impact on net income attributed to shareholders resulting from an immediate 10%, 20% and 30% change in market values of publicly traded equities followed by a return to the expected level of growth assumed in the valuation of policy liabilities, excluding impacts from asset-based fees earned on assets under management and policyholder account value. (3) Please refer to “Sensitivity of Earnings to Changes in Assumptions” section below for more information on the level of growth assumed and on the net income sensitivity to changes in these long-term assumptions. (4) Defined as earnings sensitivity to a change in public equity markets including settlements on reinsurance contracts, but before the offset of hedge assets or other risk mitigants. (5) This impact for general fund equity investments includes general fund investments supporting our policy liabilities, investment in seed money investments (in segregated and mutual funds made by Corporate and Other segment) and the impact on policy liabilities related to the projected future fee income on variable universal life and other unit linked products. The impact does not include: (i) any potential impact on public equity weightings; (ii) any gains or losses on AFS public equities held in the Corporate and Other segment; or (iii) any gains or losses on public equity investments held in Manulife Bank. The participating policy funds are largely self-supporting and generate no material impact on net income attributed to shareholders as a result of changes in equity markets. (6) Includes the impact of rebalancing equity hedges in the macro and dynamic hedging program. The impact of dynamic hedge rebalancing represents the impact of rebalancing equity hedges for dynamically hedged variable annuity guarantee best estimate liabilities at 5% intervals but does not include any impact in respect of other sources of hedge ineffectiveness (e.g. fund tracking, realized volatility and equity, interest rate correlations different from expected among other factors). (7) The sensitivity on net income attributed to shareholders from changes in public equity returns after the impact of hedging is largely unchanged as at December 31, 2022 compared with December 31, 2021. This is primarily driven by the decline in sensitivities in 1Q22 as a result of the U.S. variable annuity reinsurance transaction being largely offset by the net increase in sensitivities from the second quarter of 2022 (“2Q22”) to 4Q22 as a result of the impact of equity market declines on our variable universal life business projected fee income. The following table shows the potential impact to MLI’s LICAT ratio resulting from changes in public equity market values. Potential immediate impact on MLI’s LICAT ratio arising from public equity returns different than the expected returns assumed in (1),(2),(3) the valuation of policy liabilities ImpactonMLI’sLICATratio Percentage points -30% -20% -10% +10% +20% +30% December 31, 2022 (1) (1) – – 1 1 December 31, 2021 (1) – – – 1 – (1) See “Caution Related to Sensitivities” above. In addition, estimates exclude changes to the net actuarial gains/losses with respect to the Company’s pension obligations as a result of changes in equity markets, as the impact on the quoted sensitivities is not considered to be material. (2) The potential impact is shown assuming that the change in value of the hedge assets does not completely offset the change in the dynamically hedged variable annuity guarantee liabilities. The estimated amount that would not be completely offset relates to our practices of not hedging the provisions for adverse deviation and of rebalancing equity hedges for dynamically hedged variable annuity liabilities at 5% intervals. (3) OSFI rules for segregated fund guarantees reflect full capital impacts of shocks over 20 quarters within a prescribed range. As such, the deterioration in equity markets could lead to further increases in capital requirements after the initial shock. Interest Rate and Spread Risk Sensitivities and Exposure Measures At December 31, 2022, we estimated the sensitivity of our net income attributed to shareholders to a 50 basis point parallel decline in interest rates to be a charge of $100 million, and to a 50 basis point parallel increase in interest rates to be a benefit of $100 million. The table below shows the potential impact on net income attributed to shareholders from a 50 basis point parallel move in interest rates. This includes a change of 50 basis points in current government, swap and corporate rates for all maturities across all markets with no change in credit spreads between government, swap and corporate rates, and with a floor of zero on government rates where government rates are not currently negative (currently zero floor applies to all countries we operate in except Japan), relative to the rates assumed in the valuation of policy liabilities, including embedded derivatives. For variable annuity guarantee liabilities that are dynamically hedged, it is assumed that interest rate hedges are rebalanced at 20 basis point intervals. 65

2022 Annual Report Page 66 Page 68

2022 Annual Report Page 66 Page 68