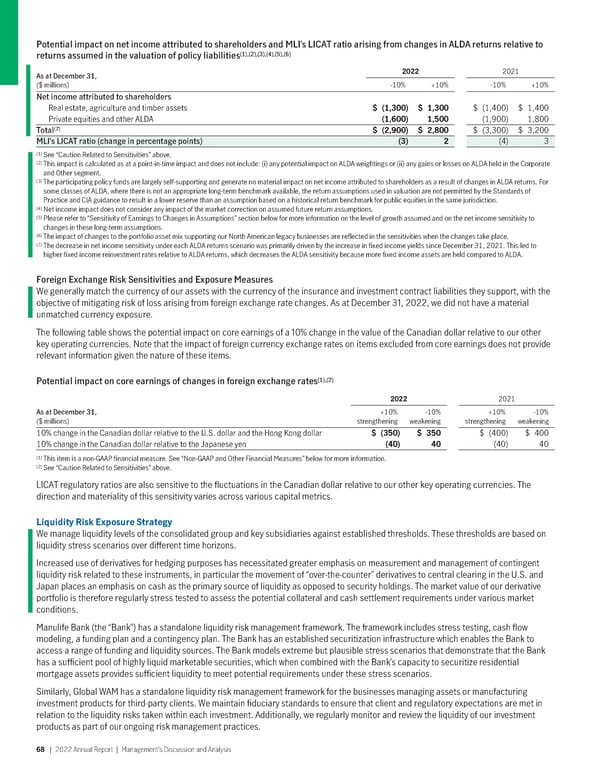

Potential impact on net income attributed to shareholders and MLI’s LICAT ratio arising from changes in ALDA returns relative to (1),(2),(3),(4),(5),(6) returns assumed in the valuation of policy liabilities As at December 31, 2022 2021 ($ millions) -10% +10% -10% +10% Net income attributed to shareholders Real estate, agriculture and timber assets $ (1,300) $ 1,300 $ (1,400) $ 1,400 Private equities and other ALDA (1,600) 1,500 (1,900) 1,800 (7) Total $ (2,900) $ 2,800 $ (3,300) $ 3,200 MLI’s LICAT ratio (change in percentage points) (3) 2 (4) 3 (1) See “Caution Related to Sensitivities” above. (2) This impact is calculated as at a point-in-time impact and does not include: (i) any potential impact on ALDA weightings or (ii) any gains or losses on ALDA held in the Corporate and Other segment. (3) The participating policy funds are largely self-supporting and generate no material impact on net income attributed to shareholders as a result of changes in ALDA returns. For some classes of ALDA, where there is not an appropriate long-term benchmark available, the return assumptions used in valuation are not permitted by the Standards of Practice and CIA guidance to result in a lower reserve than an assumption based on a historical return benchmark for public equities in the same jurisdiction. (4) Net income impact does not consider any impact of the market correction on assumed future return assumptions. (5) Please refer to “Sensitivity of Earnings to Changes in Assumptions” section below for more information on the level of growth assumed and on the net income sensitivity to changes in these long-term assumptions. (6) The impact of changes to the portfolio asset mix supporting our North American legacy businesses are reflected in the sensitivities when the changes take place. (7) The decrease in net income sensitivity under each ALDA returns scenario was primarily driven by the increase in fixed income yields since December 31, 2021. This led to higher fixed income reinvestment rates relative to ALDA returns, which decreases the ALDA sensitivity because more fixed income assets are held compared to ALDA. Foreign Exchange Risk Sensitivities and Exposure Measures We generally match the currency of our assets with the currency of the insurance and investment contract liabilities they support, with the objective of mitigating risk of loss arising from foreign exchange rate changes. As at December 31, 2022, we did not have a material unmatched currency exposure. The following table shows the potential impact on core earnings of a 10% change in the value of the Canadian dollar relative to our other key operating currencies. Note that the impact of foreign currency exchange rates on items excluded from core earnings does not provide relevant information given the nature of these items. (1),(2) Potential impact on core earnings of changes in foreign exchange rates 2022 2021 As at December 31, +10% -10% +10% -10% ($ millions) strengthening weakening strengthening weakening 10% change in the Canadian dollar relative to the U.S. dollar and the Hong Kong dollar $ (350) $ 350 $ (400) $ 400 10% change in the Canadian dollar relative to the Japanese yen (40) 40 (40) 40 (1) This item is a non-GAAP financial measure. See “Non-GAAP and Other Financial Measures” below for more information. (2) See “Caution Related to Sensitivities” above. LICAT regulatory ratios are also sensitive to the fluctuations in the Canadian dollar relative to our other key operating currencies. The direction and materiality of this sensitivity varies across various capital metrics. LiquidityRiskExposureStrategy We manage liquidity levels of the consolidated group and key subsidiaries against established thresholds. These thresholds are based on liquidity stress scenarios over different time horizons. Increased use of derivatives for hedging purposes has necessitated greater emphasis on measurement and management of contingent liquidity risk related to these instruments, in particular the movement of “over-the-counter” derivatives to central clearing in the U.S. and Japan places an emphasis on cash as the primary source of liquidity as opposed to security holdings. The market value of our derivative portfolio is therefore regularly stress tested to assess the potential collateral and cash settlement requirements under various market conditions. Manulife Bank (the “Bank”) has a standalone liquidity risk management framework. The framework includes stress testing, cash flow modeling, a funding plan and a contingency plan. The Bank has an established securitization infrastructure which enables the Bank to access a range of funding and liquidity sources. The Bank models extreme but plausible stress scenarios that demonstrate that the Bank has a sufficient pool of highly liquid marketable securities, which when combined with the Bank’s capacity to securitize residential mortgage assets provides sufficient liquidity to meet potential requirements under these stress scenarios. Similarly, Global WAM has a standalone liquidity risk management framework for the businesses managing assets or manufacturing investment products for third-party clients. We maintain fiduciary standards to ensure that client and regulatory expectations are met in relation to the liquidity risks taken within each investment. Additionally, we regularly monitor and review the liquidity of our investment products as part of our ongoing risk management practices. 68 | 2022AnnualReport | Management’sDiscussionandAnalysis

2022 Annual Report Page 69 Page 71

2022 Annual Report Page 69 Page 71