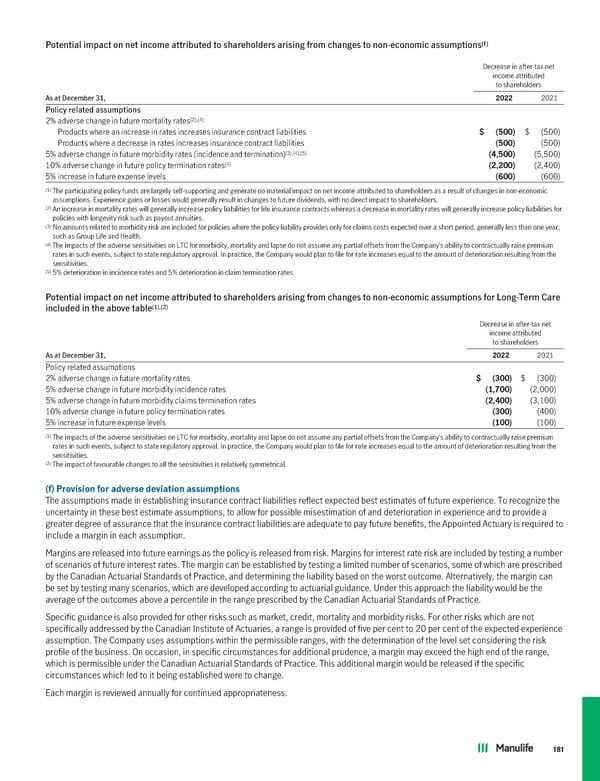

(1) Potential impact on net income attributed to shareholders arising from changes to non-economic assumptions Decrease in after-tax net income attributed to shareholders As at December 31, 2022 2021 Policy related assumptions (2),(4) 2% adverse change in future mortality rates Products where an increase in rates increases insurance contract liabilities $ (500) $ (500) Products where a decrease in rates increases insurance contract liabilities (500) (500) (3),(4),(5) 5% adverse change in future morbidity rates (incidence and termination) (4,500) (5,500) (4) 10% adverse change in future policy termination rates (2,200) (2,400) 5% increase in future expense levels (600) (600) (1) The participating policy funds are largely self-supporting and generate no material impact on net income attributed to shareholders as a result of changes in non-economic assumptions. Experience gains or losses would generally result in changes to future dividends, with no direct impact to shareholders. (2) An increase in mortality rates will generally increase policy liabilities for life insurance contracts whereas a decrease in mortality rates will generally increase policy liabilities for policies with longevity risk such as payout annuities. (3) No amounts related to morbidity risk are included for policies where the policy liability provides only for claims costs expected over a short period, generally less than one year, such as Group Life and Health. (4) The impacts of the adverse sensitivities on LTC for morbidity, mortality and lapse do not assume any partial offsets from the Company’s ability to contractually raise premium rates in such events, subject to state regulatory approval. In practice, the Company would plan to file for rate increases equal to the amount of deterioration resulting from the sensitivities. (5) 5% deterioration in incidence rates and 5% deterioration in claim termination rates. Potential impact on net income attributed to shareholders arising from changes to non-economic assumptions for Long-Term Care (1),(2) included in the above table Decrease in after-tax net income attributed to shareholders As at December 31, 2022 2021 Policy related assumptions 2% adverse change in future mortality rates $ (300) $ (300) 5% adverse change in future morbidity incidence rates (1,700) (2,000) 5% adverse change in future morbidity claims termination rates (2,400) (3,100) 10% adverse change in future policy termination rates (300) (400) 5% increase in future expense levels (100) (100) (1) The impacts of the adverse sensitivities on LTC for morbidity, mortality and lapse do not assume any partial offsets from the Company’s ability to contractually raise premium rates in such events, subject to state regulatory approval. In practice, the Company would plan to file for rate increases equal to the amount of deterioration resulting from the sensitivities. (2) The impact of favourable changes to all the sensitivities is relatively symmetrical. (f) Provision for adversedeviationassumptions The assumptions made in establishing insurance contract liabilities reflect expected best estimates of future experience. To recognize the uncertainty in these best estimate assumptions, to allow for possible misestimation of and deterioration in experience and to provide a greater degree of assurance that the insurance contract liabilities are adequate to pay future benefits, the Appointed Actuary is required to include a margin in each assumption. Margins are released into future earnings as the policy is released from risk. Margins for interest rate risk are included by testing a number of scenarios of future interest rates. The margin can be established by testing a limited number of scenarios, some of which are prescribed by the Canadian Actuarial Standards of Practice, and determining the liability based on the worst outcome. Alternatively, the margin can be set by testing many scenarios, which are developed according to actuarial guidance. Under this approach the liability would be the average of the outcomes above a percentile in the range prescribed by the Canadian Actuarial Standards of Practice. Specific guidance is also provided for other risks such as market, credit, mortality and morbidity risks. For other risks which are not specifically addressed by the Canadian Institute of Actuaries, a range is provided of five per cent to 20 per cent of the expected experience assumption. The Company uses assumptions within the permissible ranges, with the determination of the level set considering the risk profile of the business. On occasion, in specific circumstances for additional prudence, a margin may exceed the high end of the range, which is permissible under the Canadian Actuarial Standards of Practice. This additional margin would be released if the specific circumstances which led to it being established were to change. Each margin is reviewed annually for continued appropriateness. 181

2022 Annual Report Page 182 Page 184

2022 Annual Report Page 182 Page 184