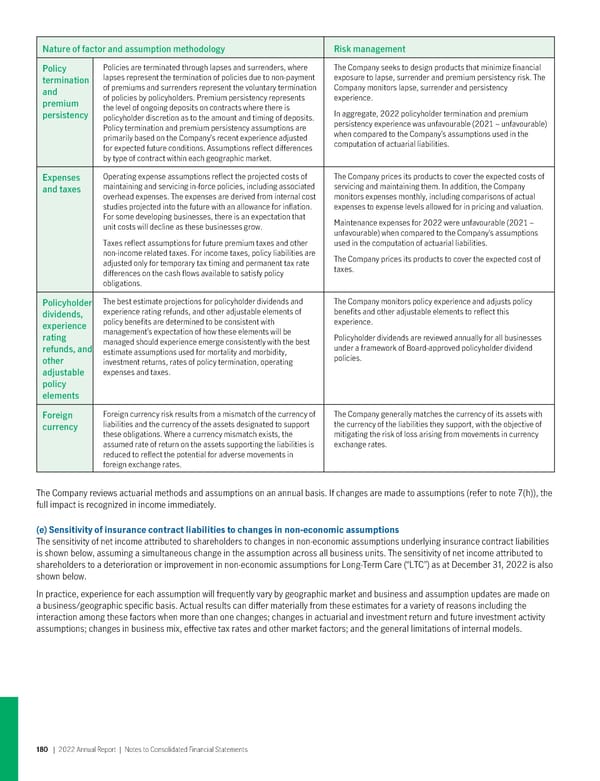

Nature of factor and assumption methodology Risk management Policy Policies are terminated through lapses and surrenders, where The Company seeks to design products that minimize financial termination lapses represent the termination of policies due to non-payment exposure to lapse, surrender and premium persistency risk. The and of premiums and surrenders represent the voluntary termination Company monitors lapse, surrender and persistency premium of policies by policyholders. Premium persistency represents experience. persistency the level of ongoing deposits on contracts where there is In aggregate, 2022 policyholder termination and premium policyholder discretion as to the amount and timing of deposits. persistency experience was unfavourable (2021 – unfavourable) Policy termination and premium persistency assumptions are when compared to the Company’s assumptions used in the primarily based on the Company’s recent experience adjusted computation of actuarial liabilities. for expected future conditions. Assumptions reflect differences by type of contract within each geographic market. Expenses Operating expense assumptions reflect the projected costs of The Company prices its products to cover the expected costs of and taxes maintaining and servicing in-force policies, including associated servicing and maintaining them. In addition, the Company overhead expenses. The expenses are derived from internal cost monitors expenses monthly, including comparisons of actual studies projected into the future with an allowance for inflation. expenses to expense levels allowed for in pricing and valuation. For some developing businesses, there is an expectation that Maintenance expenses for 2022 were unfavourable (2021 – unit costs will decline as these businesses grow. unfavourable) when compared to the Company’s assumptions Taxes reflect assumptions for future premium taxes and other used in the computation of actuarial liabilities. non-income related taxes. For income taxes, policy liabilities are The Company prices its products to cover the expected cost of adjusted only for temporary tax timing and permanent tax rate taxes. differences on the cash flows available to satisfy policy obligations. Policyholder The best estimate projections for policyholder dividends and The Company monitors policy experience and adjusts policy dividends, experience rating refunds, and other adjustable elements of benefits and other adjustable elements to reflect this experience policy benefits are determined to be consistent with experience. rating management’s expectation of how these elements will be Policyholder dividends are reviewed annually for all businesses refunds, and managed should experience emerge consistently with the best under a framework of Board-approved policyholder dividend estimate assumptions used for mortality and morbidity, policies. other investment returns, rates of policy termination, operating adjustable expenses and taxes. policy elements Foreign Foreign currency risk results from a mismatch of the currency of The Company generally matches the currency of its assets with currency liabilities and the currency of the assets designated to support the currency of the liabilities they support, with the objective of these obligations. Where a currency mismatch exists, the mitigating the risk of loss arising from movements in currency assumed rate of return on the assets supporting the liabilities is exchange rates. reduced to reflect the potential for adverse movements in foreign exchange rates. The Company reviews actuarial methods and assumptions on an annual basis. If changes are made to assumptions (refer to note 7(h)), the full impact is recognized in income immediately. (e) Sensitivity of insurancecontractliabilitiestochangesinnon-economicassumptions The sensitivity of net income attributed to shareholders to changes in non-economic assumptions underlying insurance contract liabilities is shown below, assuming a simultaneous change in the assumption across all business units. The sensitivity of net income attributed to shareholders to a deterioration or improvement in non-economic assumptions for Long-Term Care (“LTC”) as at December 31, 2022 is also shown below. In practice, experience for each assumption will frequently vary by geographic market and business and assumption updates are made on a business/geographic specific basis. Actual results can differ materially from these estimates for a variety of reasons including the interaction among these factors when more than one changes; changes in actuarial and investment return and future investment activity assumptions; changes in business mix, effective tax rates and other market factors; and the general limitations of internal models. 180 | 2022AnnualReport | NotestoConsolidatedFinancialStatements

2022 Annual Report Page 181 Page 183

2022 Annual Report Page 181 Page 183