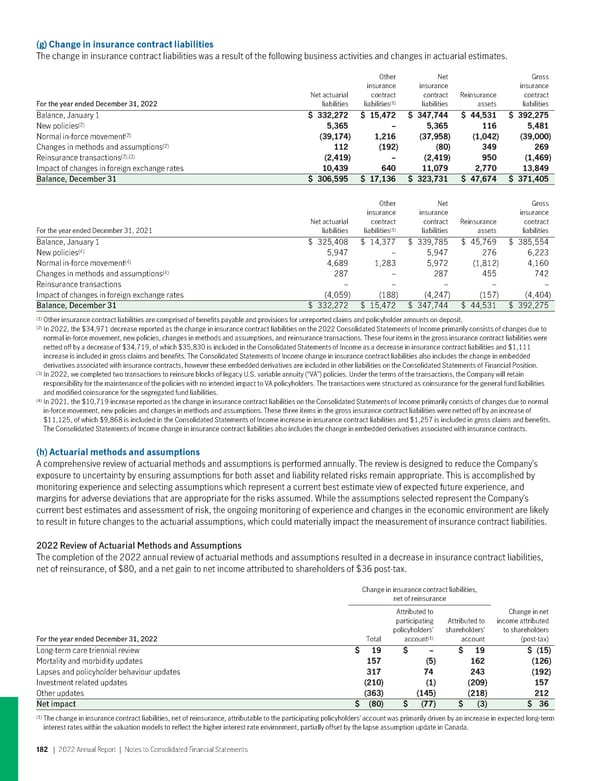

(g) Changeininsurancecontractliabilities The change in insurance contract liabilities was a result of the following business activities and changes in actuarial estimates. Other Net Gross insurance insurance insurance Net actuarial contract contract Reinsurance contract For the year ended December 31, 2022 liabilities (1) liabilities liabilities assets liabilities Balance, January 1 $ 332,272 $ 15,472 $ 347,744 $ 44,531 $ 392,275 (2) New policies 5,365 – 5,365 116 5,481 (2) Normal in-force movement (39,174) 1,216 (37,958) (1,042) (39,000) (2) Changes in methods and assumptions 112 (192) (80) 349 269 (2),(3) Reinsurance transactions (2,419) – (2,419) 950 (1,469) Impact of changes in foreign exchange rates 10,439 640 11,079 2,770 13,849 Balance, December 31 $ 306,595 $ 17,136 $ 323,731 $ 47,674 $ 371,405 Other Net Gross insurance insurance insurance Net actuarial contract contract Reinsurance contract For the year ended December 31, 2021 liabilities (1) liabilities liabilities assets liabilities Balance, January 1 $ 325,408 $ 14,377 $ 339,785 $ 45,769 $ 385,554 (4) New policies 5,947 – 5,947 276 6,223 (4) Normal in-force movement 4,689 1,283 5,972 (1,812) 4,160 (4) Changes in methods and assumptions 287 – 287 455 742 Reinsurance transactions – – – – – Impact of changes in foreign exchange rates (4,059) (188) (4,247) (157) (4,404) Balance, December 31 $ 332,272 $ 15,472 $ 347,744 $ 44,531 $ 392,275 (1) Other insurance contract liabilities are comprised of benefits payable and provisions for unreported claims and policyholder amounts on deposit. (2) In 2022, the $34,971 decrease reported as the change in insurance contract liabilities on the 2022 Consolidated Statements of Income primarily consists of changes due to normal in-force movement, new policies, changes in methods and assumptions, and reinsurance transactions. These four items in the gross insurance contract liabilities were netted off by a decrease of $34,719, of which $35,830 is included in the Consolidated Statements of Income as a decrease in insurance contract liabilities and $1,111 increase is included in gross claims and benefits. The Consolidated Statements of Income change in insurance contract liabilities also includes the change in embedded derivatives associated with insurance contracts, however these embedded derivatives are included in other liabilities on the Consolidated Statements of Financial Position. (3) In 2022, we completed two transactions to reinsure blocks of legacy U.S. variable annuity (“VA”) policies. Under the terms of the transactions, the Company will retain responsibility for the maintenance of the policies with no intended impact to VA policyholders. The transactions were structured as coinsurance for the general fund liabilities and modified coinsurance for the segregated fund liabilities. (4) In 2021, the $10,719 increase reported as the change in insurance contract liabilities on the Consolidated Statements of Income primarily consists of changes due to normal in-force movement, new policies and changes in methods and assumptions. These three items in the gross insurance contract liabilities were netted off by an increase of $11,125, of which $9,868 is included in the Consolidated Statements of Income increase in insurance contract liabilities and $1,257 is included in gross claims and benefits. The Consolidated Statements of Income change in insurance contract liabilities also includes the change in embedded derivatives associated with insurance contracts. (h) Actuarialmethodsandassumptions A comprehensive review of actuarial methods and assumptions is performed annually. The review is designed to reduce the Company’s exposure to uncertainty by ensuring assumptions for both asset and liability related risks remain appropriate. This is accomplished by monitoring experience and selecting assumptions which represent a current best estimate view of expected future experience, and margins for adverse deviations that are appropriate for the risks assumed. While the assumptions selected represent the Company’s current best estimates and assessment of risk, the ongoing monitoring of experience and changes in the economic environment are likely to result in future changes to the actuarial assumptions, which could materially impact the measurement of insurance contract liabilities. 2022 Review of Actuarial Methods and Assumptions The completion of the 2022 annual review of actuarial methods and assumptions resulted in a decrease in insurance contract liabilities, net of reinsurance, of $80, and a net gain to net income attributed to shareholders of $36 post-tax. Change in insurance contract liabilities, net of reinsurance Attributed to Change in net participating Attributed to income attributed policyholders’ shareholders’ to shareholders For the year ended December 31, 2022 Total (1) account account (post-tax) Long-term care triennial review $ 19 $ – $ 19 $ (15) Mortality and morbidity updates 157 (5) 162 (126) Lapses and policyholder behaviour updates 317 74 243 (192) Investment related updates (210) (1) (209) 157 Other updates (363) (145) (218) 212 Net impact $ (80) $ (77) $ (3) $ 36 (1) The change in insurance contract liabilities, net of reinsurance, attributable to the participating policyholders’ account was primarily driven by an increase in expected long-term interest rates within the valuation models to reflect the higher interest rate environment, partially offset by the lapse assumption update in Canada. 182 | 2022AnnualReport | NotestoConsolidatedFinancialStatements

2022 Annual Report Page 183 Page 185

2022 Annual Report Page 183 Page 185