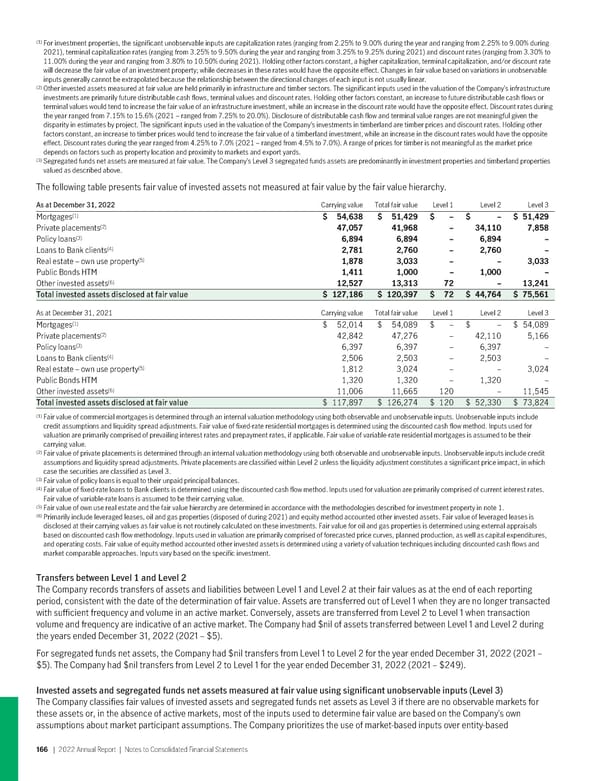

(1) For investment properties, the significant unobservable inputs are capitalization rates (ranging from 2.25% to 9.00% during the year and ranging from 2.25% to 9.00% during 2021), terminal capitalization rates (ranging from 3.25% to 9.50% during the year and ranging from 3.25% to 9.25% during 2021) and discount rates (ranging from 3.30% to 11.00% during the year and ranging from 3.80% to 10.50% during 2021). Holding other factors constant, a higher capitalization, terminal capitalization, and/or discount rate will decrease the fair value of an investment property; while decreases in these rates would have the opposite effect. Changes in fair value based on variations in unobservable inputs generally cannot be extrapolated because the relationship between the directional changes of each input is not usually linear. (2) Other invested assets measured at fair value are held primarily in infrastructure and timber sectors. The significant inputs used in the valuation of the Company’s infrastructure investments are primarily future distributable cash flows, terminal values and discount rates. Holding other factors constant, an increase to future distributable cash flows or terminal values would tend to increase the fair value of an infrastructure investment, while an increase in the discount rate would have the opposite effect. Discount rates during the year ranged from 7.15% to 15.6% (2021 – ranged from 7.25% to 20.0%). Disclosure of distributable cash flow and terminal value ranges are not meaningful given the disparity in estimates by project. The significant inputs used in the valuation of the Company’s investments in timberland are timber prices and discount rates. Holding other factors constant, an increase to timber prices would tend to increase the fair value of a timberland investment, while an increase in the discount rates would have the opposite effect. Discount rates during the year ranged from 4.25% to 7.0% (2021 – ranged from 4.5% to 7.0%). A range of prices for timber is not meaningful as the market price depends on factors such as property location and proximity to markets and export yards. (3) Segregated funds net assets are measured at fair value. The Company’s Level 3 segregated funds assets are predominantly in investment properties and timberland properties valued as described above. The following table presents fair value of invested assets not measured at fair value by the fair value hierarchy. As at December 31, 2022 Carrying value Total fair value Level 1 Level 2 Level 3 (1) Mortgages $ 54,638 $ 51,429 $ – $ – $ 51,429 (2) Private placements 47,057 41,968 – 34,110 7,858 (3) Policy loans 6,894 6,894 – 6,894 – (4) Loans to Bank clients 2,781 2,760 – 2,760 – (5) Real estate – own use property 1,878 3,033 – – 3,033 Public Bonds HTM 1,411 1,000 – 1,000 – (6) Other invested assets 12,527 13,313 72 – 13,241 Total invested assets disclosed at fair value $ 127,186 $ 120,397 $ 72 $ 44,764 $ 75,561 As at December 31, 2021 Carrying value Total fair value Level 1 Level 2 Level 3 (1) Mortgages $ 52,014 $ 54,089 $ – $ – $ 54,089 (2) Private placements 42,842 47,276 – 42,110 5,166 (3) Policy loans 6,397 6,397 – 6,397 – (4) Loans to Bank clients 2,506 2,503 – 2,503 – (5) Real estate – own use property 1,812 3,024 – – 3,024 Public Bonds HTM 1,320 1,320 – 1,320 – (6) Other invested assets 11,006 11,665 120 – 11,545 Total invested assets disclosed at fair value $ 117,897 $ 126,274 $ 120 $ 52,330 $ 73,824 (1) Fair value of commercial mortgages is determined through an internal valuation methodology using both observable and unobservable inputs. Unobservable inputs include credit assumptions and liquidity spread adjustments. Fair value of fixed-rate residential mortgages is determined using the discounted cash flow method. Inputs used for valuation are primarily comprised of prevailing interest rates and prepayment rates, if applicable. Fair value of variable-rate residential mortgages is assumed to be their carrying value. (2) Fair value of private placements is determined through an internal valuation methodology using both observable and unobservable inputs. Unobservable inputs include credit assumptions and liquidity spread adjustments. Private placements are classified within Level 2 unless the liquidity adjustment constitutes a significant price impact, in which case the securities are classified as Level 3. (3) Fair value of policy loans is equal to their unpaid principal balances. (4) Fair value of fixed-rate loans to Bank clients is determined using the discounted cash flow method. Inputs used for valuation are primarily comprised of current interest rates. Fair value of variable-rate loans is assumed to be their carrying value. (5) Fair value of own use real estate and the fair value hierarchy are determined in accordance with the methodologies described for investment property in note 1. (6) Primarily include leveraged leases, oil and gas properties (disposed of during 2021) and equity method accounted other invested assets. Fair value of leveraged leases is disclosed at their carrying values as fair value is not routinely calculated on these investments. Fair value for oil and gas properties is determined using external appraisals based on discounted cash flow methodology. Inputs used in valuation are primarily comprised of forecasted price curves, planned production, as well as capital expenditures, and operating costs. Fair value of equity method accounted other invested assets is determined using a variety of valuation techniques including discounted cash flows and market comparable approaches. Inputs vary based on the specific investment. Transfers between Level 1 and Level 2 The Company records transfers of assets and liabilities between Level 1 and Level 2 at their fair values as at the end of each reporting period, consistent with the date of the determination of fair value. Assets are transferred out of Level 1 when they are no longer transacted with sufficient frequency and volume in an active market. Conversely, assets are transferred from Level 2 to Level 1 when transaction volume and frequency are indicative of an active market. The Company had $nil of assets transferred between Level 1 and Level 2 during the years ended December 31, 2022 (2021 – $5). For segregated funds net assets, the Company had $nil transfers from Level 1 to Level 2 for the year ended December 31, 2022 (2021 – $5). The Company had $nil transfers from Level 2 to Level 1 for the year ended December 31, 2022 (2021 – $249). Invested assets and segregated funds net assets measured at fair value using significant unobservable inputs (Level 3) The Company classifies fair values of invested assets and segregated funds net assets as Level 3 if there are no observable markets for these assets or, in the absence of active markets, most of the inputs used to determine fair value are based on the Company’s own assumptions about market participant assumptions. The Company prioritizes the use of market-based inputs over entity-based 166 | 2022AnnualReport | NotestoConsolidatedFinancialStatements

2022 Annual Report Page 167 Page 169

2022 Annual Report Page 167 Page 169