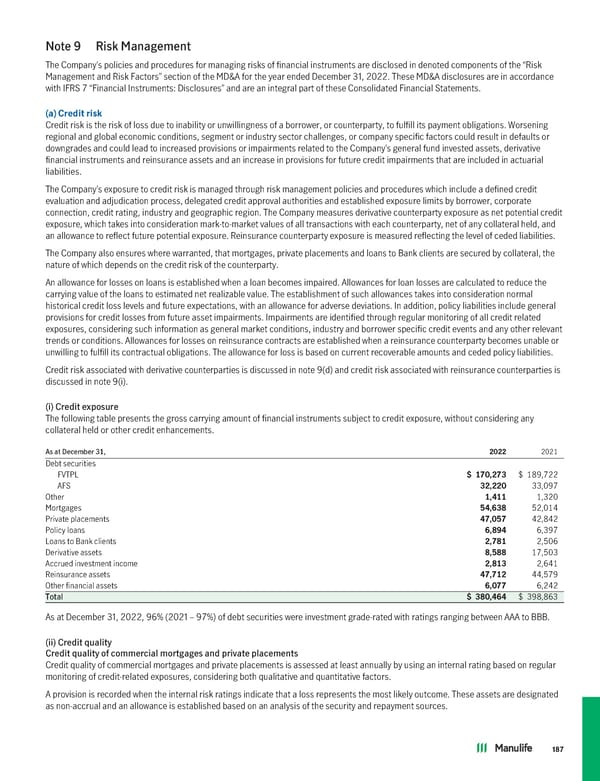

Note 9 Risk Management The Company’s policies and procedures for managing risks of financial instruments are disclosed in denoted components of the “Risk Management and Risk Factors” section of the MD&A for the year ended December 31, 2022. These MD&A disclosures are in accordance with IFRS 7 “Financial Instruments: Disclosures” and are an integral part of these Consolidated Financial Statements. (a) Credit risk Credit risk is the risk of loss due to inability or unwillingness of a borrower, or counterparty, to fulfill its payment obligations. Worsening regional and global economic conditions, segment or industry sector challenges, or company specific factors could result in defaults or downgrades and could lead to increased provisions or impairments related to the Company’s general fund invested assets, derivative financial instruments and reinsurance assets and an increase in provisions for future credit impairments that are included in actuarial liabilities. The Company’s exposure to credit risk is managed through risk management policies and procedures which include a defined credit evaluation and adjudication process, delegated credit approval authorities and established exposure limits by borrower, corporate connection, credit rating, industry and geographic region. The Company measures derivative counterparty exposure as net potential credit exposure, which takes into consideration mark-to-market values of all transactions with each counterparty, net of any collateral held, and an allowance to reflect future potential exposure. Reinsurance counterparty exposure is measured reflecting the level of ceded liabilities. The Company also ensures where warranted, that mortgages, private placements and loans to Bank clients are secured by collateral, the nature of which depends on the credit risk of the counterparty. An allowance for losses on loans is established when a loan becomes impaired. Allowances for loan losses are calculated to reduce the carrying value of the loans to estimated net realizable value. The establishment of such allowances takes into consideration normal historical credit loss levels and future expectations, with an allowance for adverse deviations. In addition, policy liabilities include general provisions for credit losses from future asset impairments. Impairments are identified through regular monitoring of all credit related exposures, considering such information as general market conditions, industry and borrower specific credit events and any other relevant trends or conditions. Allowances for losses on reinsurance contracts are established when a reinsurance counterparty becomes unable or unwilling to fulfill its contractual obligations. The allowance for loss is based on current recoverable amounts and ceded policy liabilities. Credit risk associated with derivative counterparties is discussed in note 9(d) and credit risk associated with reinsurance counterparties is discussed in note 9(i). (i) Credit exposure The following table presents the gross carrying amount of financial instruments subject to credit exposure, without considering any collateral held or other credit enhancements. As at December 31, 2022 2021 Debt securities FVTPL $ 170,273 $ 189,722 AFS 32,220 33,097 Other 1,411 1,320 Mortgages 54,638 52,014 Private placements 47,057 42,842 Policy loans 6,894 6,397 Loans to Bank clients 2,781 2,506 Derivative assets 8,588 17,503 Accrued investment income 2,813 2,641 Reinsurance assets 47,712 44,579 Other financial assets 6,077 6,242 Total $ 380,464 $ 398,863 As at December 31, 2022, 96% (2021 – 97%) of debt securities were investment grade-rated with ratings ranging between AAA to BBB. (ii) Credit quality Credit quality of commercial mortgages and private placements Credit quality of commercial mortgages and private placements is assessed at least annually by using an internal rating based on regular monitoring of credit-related exposures, considering both qualitative and quantitative factors. A provision is recorded when the internal risk ratings indicate that a loss represents the most likely outcome. These assets are designated as non-accrual and an allowance is established based on an analysis of the security and repayment sources. 187

2022 Annual Report Page 188 Page 190

2022 Annual Report Page 188 Page 190