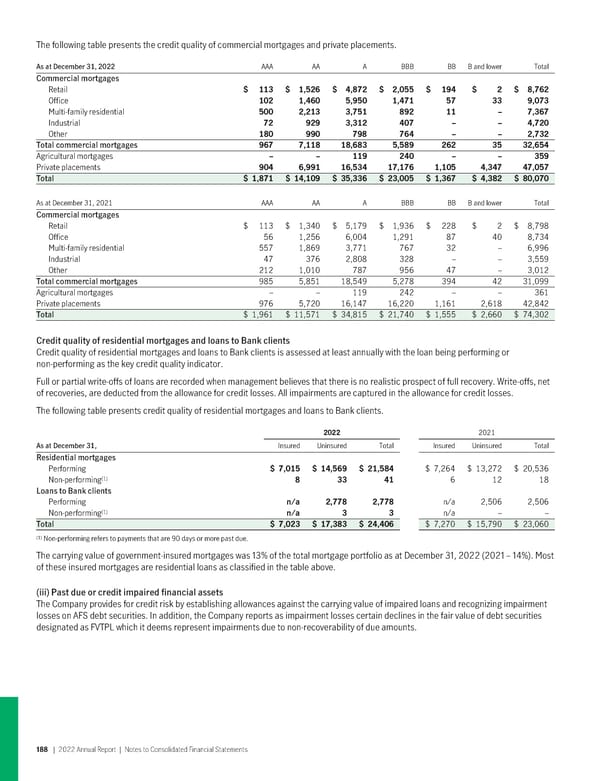

The following table presents the credit quality of commercial mortgages and private placements. As at December 31, 2022 AAA AA A BBB BB B and lower Total Commercial mortgages Retail $ 113 $ 1,526 $ 4,872 $ 2,055 $ 194 $ 2 $ 8,762 Office 102 1,460 5,950 1,471 57 33 9,073 Multi-family residential 500 2,213 3,751 892 11 – 7,367 Industrial 72 929 3,312 407 – – 4,720 Other 180 990 798 764 – – 2,732 Total commercial mortgages 967 7,118 18,683 5,589 262 35 32,654 Agricultural mortgages – – 119 240 – – 359 Private placements 904 6,991 16,534 17,176 1,105 4,347 47,057 Total $ 1,871 $ 14,109 $ 35,336 $ 23,005 $ 1,367 $ 4,382 $ 80,070 As at December 31, 2021 AAA AA A BBB BB B and lower Total Commercial mortgages Retail $ 113 $ 1,340 $ 5,179 $ 1,936 $ 228 $ 2 $ 8,798 Office 56 1,256 6,004 1,291 87 40 8,734 Multi-family residential 557 1,869 3,771 767 32 – 6,996 Industrial 47 376 2,808 328 – – 3,559 Other 212 1,010 787 956 47 – 3,012 Total commercial mortgages 985 5,851 18,549 5,278 394 42 31,099 Agricultural mortgages – – 119 242 – – 361 Private placements 976 5,720 16,147 16,220 1,161 2,618 42,842 Total $ 1,961 $ 11,571 $ 34,815 $ 21,740 $ 1,555 $ 2,660 $ 74,302 Credit quality of residential mortgages and loans to Bank clients Credit quality of residential mortgages and loans to Bank clients is assessed at least annually with the loan being performing or non-performing as the key credit quality indicator. Full or partial write-offs of loans are recorded when management believes that there is no realistic prospect of full recovery. Write-offs, net of recoveries, are deducted from the allowance for credit losses. All impairments are captured in the allowance for credit losses. The following table presents credit quality of residential mortgages and loans to Bank clients. 2022 2021 As at December 31, Insured Uninsured Total Insured Uninsured Total Residential mortgages Performing $ 7,015 $ 14,569 $ 21,584 $ 7,264 $ 13,272 $ 20,536 (1) Non-performing 83341 6 12 18 Loans to Bank clients Performing n/a 2,778 2,778 n/a 2,506 2,506 (1) Non-performing n/a 3 3 n/a – – Total $ 7,023 $ 17,383 $ 24,406 $ 7,270 $ 15,790 $ 23,060 (1) Non-performing refers to payments that are 90 days or more past due. The carrying value of government-insured mortgages was 13% of the total mortgage portfolio as at December 31, 2022 (2021 – 14%). Most of these insured mortgages are residential loans as classified in the table above. (iii) Past due or credit impaired financial assets The Company provides for credit risk by establishing allowances against the carrying value of impaired loans and recognizing impairment losses on AFS debt securities. In addition, the Company reports as impairment losses certain declines in the fair value of debt securities designated as FVTPL which it deems represent impairments due to non-recoverability of due amounts. 188 | 2022AnnualReport | NotestoConsolidatedFinancialStatements

2022 Annual Report Page 189 Page 191

2022 Annual Report Page 189 Page 191