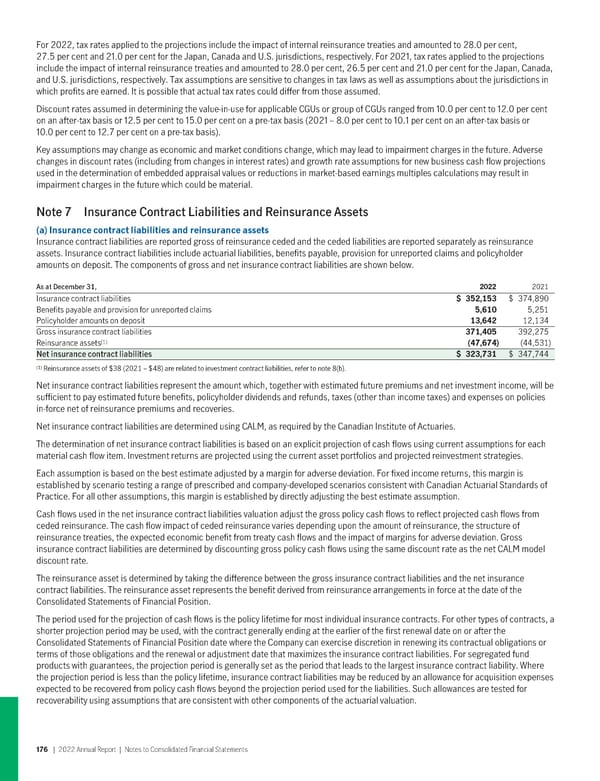

For 2022, tax rates applied to the projections include the impact of internal reinsurance treaties and amounted to 28.0 per cent, 27.5 per cent and 21.0 per cent for the Japan, Canada and U.S. jurisdictions, respectively. For 2021, tax rates applied to the projections include the impact of internal reinsurance treaties and amounted to 28.0 per cent, 26.5 per cent and 21.0 per cent for the Japan, Canada, and U.S. jurisdictions, respectively. Tax assumptions are sensitive to changes in tax laws as well as assumptions about the jurisdictions in which profits are earned. It is possible that actual tax rates could differ from those assumed. Discount rates assumed in determining the value-in-use for applicable CGUs or group of CGUs ranged from 10.0 per cent to 12.0 per cent on an after-tax basis or 12.5 per cent to 15.0 per cent on a pre-tax basis (2021 – 8.0 per cent to 10.1 per cent on an after-tax basis or 10.0 per cent to 12.7 per cent on a pre-tax basis). Key assumptions may change as economic and market conditions change, which may lead to impairment charges in the future. Adverse changes in discount rates (including from changes in interest rates) and growth rate assumptions for new business cash flow projections used in the determination of embedded appraisal values or reductions in market-based earnings multiples calculations may result in impairment charges in the future which could be material. Note 7 Insurance Contract Liabilities and Reinsurance Assets (a) Insurancecontractliabilitiesandreinsuranceassets Insurance contract liabilities are reported gross of reinsurance ceded and the ceded liabilities are reported separately as reinsurance assets. Insurance contract liabilities include actuarial liabilities, benefits payable, provision for unreported claims and policyholder amounts on deposit. The components of gross and net insurance contract liabilities are shown below. As at December 31, 2022 2021 Insurance contract liabilities $ 352,153 $ 374,890 Benefits payable and provision for unreported claims 5,610 5,251 Policyholder amounts on deposit 13,642 12,134 Gross insurance contract liabilities 371,405 392,275 (1) Reinsurance assets (47,674) (44,531) Net insurance contract liabilities $ 323,731 $ 347,744 (1) Reinsurance assets of $38 (2021 – $48) are related to investment contract liabilities, refer to note 8(b). Net insurance contract liabilities represent the amount which, together with estimated future premiums and net investment income, will be sufficient to pay estimated future benefits, policyholder dividends and refunds, taxes (other than income taxes) and expenses on policies in-force net of reinsurance premiums and recoveries. Net insurance contract liabilities are determined using CALM, as required by the Canadian Institute of Actuaries. The determination of net insurance contract liabilities is based on an explicit projection of cash flows using current assumptions for each material cash flow item. Investment returns are projected using the current asset portfolios and projected reinvestment strategies. Each assumption is based on the best estimate adjusted by a margin for adverse deviation. For fixed income returns, this margin is established by scenario testing a range of prescribed and company-developed scenarios consistent with Canadian Actuarial Standards of Practice. For all other assumptions, this margin is established by directly adjusting the best estimate assumption. Cash flows used in the net insurance contract liabilities valuation adjust the gross policy cash flows to reflect projected cash flows from ceded reinsurance. The cash flow impact of ceded reinsurance varies depending upon the amount of reinsurance, the structure of reinsurance treaties, the expected economic benefit from treaty cash flows and the impact of margins for adverse deviation. Gross insurance contract liabilities are determined by discounting gross policy cash flows using the same discount rate as the net CALM model discount rate. The reinsurance asset is determined by taking the difference between the gross insurance contract liabilities and the net insurance contract liabilities. The reinsurance asset represents the benefit derived from reinsurance arrangements in force at the date of the Consolidated Statements of Financial Position. The period used for the projection of cash flows is the policy lifetime for most individual insurance contracts. For other types of contracts, a shorter projection period may be used, with the contract generally ending at the earlier of the first renewal date on or after the Consolidated Statements of Financial Position date where the Company can exercise discretion in renewing its contractual obligations or terms of those obligations and the renewal or adjustment date that maximizes the insurance contract liabilities. For segregated fund products with guarantees, the projection period is generally set as the period that leads to the largest insurance contract liability. Where the projection period is less than the policy lifetime, insurance contract liabilities may be reduced by an allowance for acquisition expenses expected to be recovered from policy cash flows beyond the projection period used for the liabilities. Such allowances are tested for recoverability using assumptions that are consistent with other components of the actuarial valuation. 176 | 2022AnnualReport | NotestoConsolidatedFinancialStatements

2022 Annual Report Page 177 Page 179

2022 Annual Report Page 177 Page 179