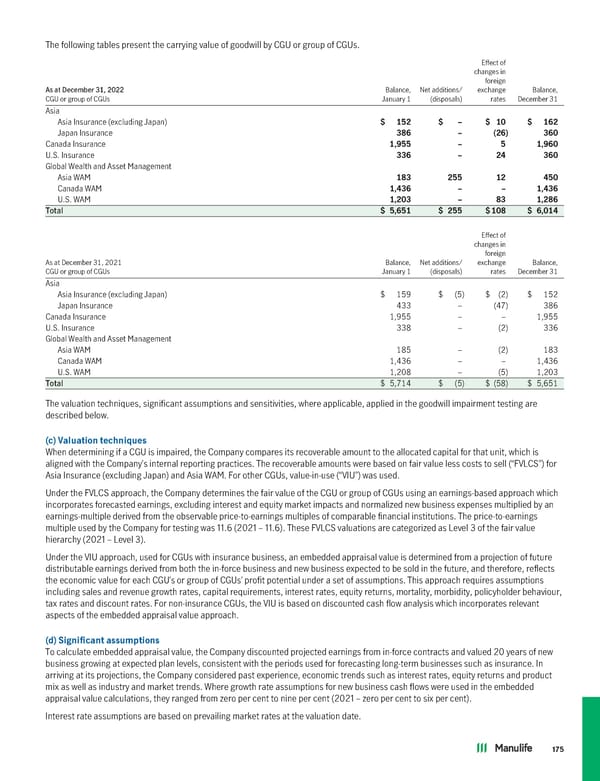

The following tables present the carrying value of goodwill by CGU or group of CGUs. Effect of changes in foreign As at December 31, 2022 Balance, Net additions/ exchange Balance, CGU or group of CGUs January 1 (disposals) rates December 31 Asia Asia Insurance (excluding Japan) $ 152 $ – $ 10 $ 162 Japan Insurance 386 – (26) 360 Canada Insurance 1,955 – 5 1,960 U.S. Insurance 336 – 24 360 Global Wealth and Asset Management Asia WAM 183 255 12 450 Canada WAM 1,436 – – 1,436 U.S. WAM 1,203 – 83 1,286 Total $ 5,651 $ 255 $108 $ 6,014 Effect of changes in foreign As at December 31, 2021 Balance, Net additions/ exchange Balance, CGU or group of CGUs January 1 (disposals) rates December 31 Asia Asia Insurance (excluding Japan) $ 159 $ (5) $ (2) $ 152 Japan Insurance 433 – (47) 386 Canada Insurance 1,955 – – 1,955 U.S. Insurance 338 – (2) 336 Global Wealth and Asset Management Asia WAM 185 – (2) 183 Canada WAM 1,436 – – 1,436 U.S. WAM 1,208 – (5) 1,203 Total $ 5,714 $ (5) $ (58) $ 5,651 The valuation techniques, significant assumptions and sensitivities, where applicable, applied in the goodwill impairment testing are described below. (c) Valuationtechniques When determining if a CGU is impaired, the Company compares its recoverable amount to the allocated capital for that unit, which is aligned with the Company’s internal reporting practices. The recoverable amounts were based on fair value less costs to sell (“FVLCS”) for Asia Insurance (excluding Japan) and Asia WAM. For other CGUs, value-in-use (“VIU”) was used. Under the FVLCS approach, the Company determines the fair value of the CGU or group of CGUs using an earnings-based approach which incorporates forecasted earnings, excluding interest and equity market impacts and normalized new business expenses multiplied by an earnings-multiple derived from the observable price-to-earnings multiples of comparable financial institutions. The price-to-earnings multiple used by the Company for testing was 11.6 (2021 – 11.6). These FVLCS valuations are categorized as Level 3 of the fair value hierarchy (2021 – Level 3). Under the VIU approach, used for CGUs with insurance business, an embedded appraisal value is determined from a projection of future distributable earnings derived from both the in-force business and new business expected to be sold in the future, and therefore, reflects the economic value for each CGU’s or group of CGUs’ profit potential under a set of assumptions. This approach requires assumptions including sales and revenue growth rates, capital requirements, interest rates, equity returns, mortality, morbidity, policyholder behaviour, tax rates and discount rates. For non-insurance CGUs, the VIU is based on discounted cash flow analysis which incorporates relevant aspects of the embedded appraisal value approach. (d) Significantassumptions To calculate embedded appraisal value, the Company discounted projected earnings from in-force contracts and valued 20 years of new business growing at expected plan levels, consistent with the periods used for forecasting long-term businesses such as insurance. In arriving at its projections, the Company considered past experience, economic trends such as interest rates, equity returns and product mix as well as industry and market trends. Where growth rate assumptions for new business cash flows were used in the embedded appraisal value calculations, they ranged from zero per cent to nine per cent (2021 – zero per cent to six per cent). Interest rate assumptions are based on prevailing market rates at the valuation date. 175

2022 Annual Report Page 176 Page 178

2022 Annual Report Page 176 Page 178