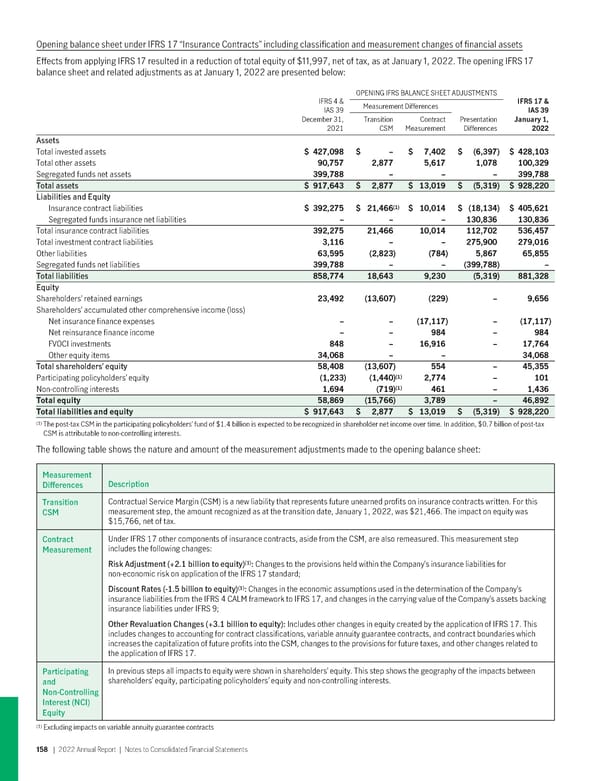

Opening balance sheet under IFRS 17 “Insurance Contracts” including classification and measurement changes of financial assets Effects from applying IFRS 17 resulted in a reduction of total equity of $11,997, net of tax, as at January 1, 2022. The opening IFRS 17 balance sheet and related adjustments as at January 1, 2022 are presented below: OPENING IFRS BALANCE SHEET ADJUSTMENTS IFRS 4 & Measurement Differences IFRS17& IAS 39 IAS39 December 31, Transition Contract Presentation January1, 2021 CSM Measurement Differences 2022 Assets Total invested assets $ 427,098 $ – $ 7,402 $ (6,397) $ 428,103 Total other assets 90,757 2,877 5,617 1,078 100,329 Segregated funds net assets 399,788 – – – 399,788 Total assets $ 917,643 $ 2,877 $ 13,019 $ (5,319) $ 928,220 Liabilities and Equity (1) Insurance contract liabilities $ 392,275 $ 21,466 $ 10,014 $ (18,134) $ 405,621 Segregated funds insurance net liabilities – – – 130,836 130,836 Total insurance contract liabilities 392,275 21,466 10,014 112,702 536,457 Total investment contract liabilities 3,116 – – 275,900 279,016 Other liabilities 63,595 (2,823) (784) 5,867 65,855 Segregated funds net liabilities 399,788 – – (399,788) – Total liabilities 858,774 18,643 9,230 (5,319) 881,328 Equity Shareholders’ retained earnings 23,492 (13,607) (229) – 9,656 Shareholders’ accumulated other comprehensive income (loss) Net insurance finance expenses – – (17,117) – (17,117) Net reinsurance finance income – – 984 – 984 FVOCI investments 848 – 16,916 – 17,764 Other equity items 34,068 – – 34,068 Total shareholders’ equity 58,408 (13,607) 554 – 45,355 (1) Participating policyholders’ equity (1,233) (1,440) 2,774 – 101 (1) Non-controlling interests 1,694 (719) 461 – 1,436 Totalequity 58,869 (15,766) 3,789 – 46,892 Totalliabilities andequity $ 917,643 $ 2,877 $ 13,019 $ (5,319) $ 928,220 (1) The post-tax CSM in the participating policyholders’ fund of $1.4 billion is expected to be recognized in shareholder net income over time. In addition, $0.7 billion of post-tax CSM is attributable to non-controlling interests. The following table shows the nature and amount of the measurement adjustments made to the opening balance sheet: Measurement Differences Description Transition Contractual Service Margin (CSM) is a new liability that represents future unearned profits on insurance contracts written. For this CSM measurement step, the amount recognized as at the transition date, January 1, 2022, was $21,466. The impact on equity was $15,766, net of tax. Contract Under IFRS 17 other components of insurance contracts, aside from the CSM, are also remeasured. This measurement step Measurement includes the following changes: (1) Risk Adjustment (+2.1 billion to equity) : Changes to the provisions held within the Company’s insurance liabilities for non-economic risk on application of the IFRS 17 standard; (1) Discount Rates (-1.5 billion to equity) : Changes in the economic assumptions used in the determination of the Company’s insurance liabilities from the IFRS 4 CALM framework to IFRS 17, and changes in the carrying value of the Company’s assets backing insurance liabilities under IFRS 9; Other Revaluation Changes (+3.1 billion to equity): Includes other changes in equity created by the application of IFRS 17. This includes changes to accounting for contract classifications, variable annuity guarantee contracts, and contract boundaries which increases the capitalization of future profits into the CSM, changes to the provisions for future taxes, and other changes related to the application of IFRS 17. Participating In previous steps all impacts to equity were shown in shareholders’ equity. This step shows the geography of the impacts between and shareholders’ equity, participating policyholders’ equity and non-controlling interests. Non-Controlling Interest (NCI) Equity (1) Excluding impacts on variable annuity guarantee contracts 158 | 2022AnnualReport | NotestoConsolidatedFinancialStatements

2022 Annual Report Page 159 Page 161

2022 Annual Report Page 159 Page 161