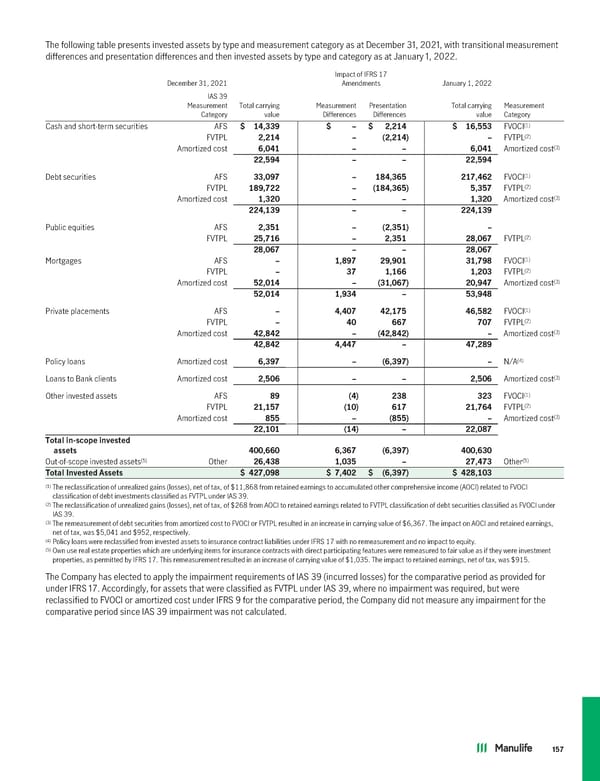

The following table presents invested assets by type and measurement category as at December 31, 2021, with transitional measurement differences and presentation differences and then invested assets by type and category as at January 1, 2022. Impact of IFRS 17 December 31, 2021 Amendments January 1, 2022 IAS 39 Measurement Total carrying Measurement Presentation Total carrying Measurement Category value Differences Differences value Category (1) Cash and short-term securities AFS $ 14,339 $ – $ 2,214 $ 16,553 FVOCI (2) FVTPL 2,214 – (2,214) – FVTPL (3) Amortized cost 6,041 – – 6,041 Amortized cost 22,594 – – 22,594 (1) Debt securities AFS 33,097 – 184,365 217,462 FVOCI (2) FVTPL 189,722 – (184,365) 5,357 FVTPL (3) Amortized cost 1,320 – – 1,320 Amortized cost 224,139 – – 224,139 Public equities AFS 2,351 – (2,351) – (2) FVTPL 25,716 – 2,351 28,067 FVTPL 28,067 – – 28,067 (1) Mortgages AFS – 1,897 29,901 31,798 FVOCI (2) FVTPL – 37 1,166 1,203 FVTPL (3) Amortized cost 52,014 – (31,067) 20,947 Amortized cost 52,014 1,934 – 53,948 (1) Private placements AFS – 4,407 42,175 46,582 FVOCI (2) FVTPL – 40 667 707 FVTPL (3) Amortized cost 42,842 – (42,842) – Amortized cost 42,842 4,447 – 47,289 (4) Policy loans Amortized cost 6,397 – (6,397) – N/A (3) Loans to Bank clients Amortized cost 2,506 – – 2,506 Amortized cost (1) Other invested assets AFS 89 (4) 238 323 FVOCI (2) FVTPL 21,157 (10) 617 21,764 FVTPL (3) Amortized cost 855 – (855) – Amortized cost 22,101 (14) – 22,087 Totalin-scopeinvested assets 400,660 6,367 (6,397) 400,630 (5) (5) Out-of-scope invested assets Other 26,438 1,035 – 27,473 Other TotalInvestedAssets $ 427,098 $ 7,402 $ (6,397) $ 428,103 (1) The reclassification of unrealized gains (losses), net of tax, of $11,868 from retained earnings to accumulated other comprehensive income (AOCI) related to FVOCI classification of debt investments classified as FVTPL under IAS 39. (2) The reclassification of unrealized gains (losses), net of tax, of $268 from AOCI to retained earnings related to FVTPL classification of debt securities classified as FVOCI under IAS 39. (3) The remeasurement of debt securities from amortized cost to FVOCI or FVTPL resulted in an increase in carrying value of $6,367. The impact on AOCI and retained earnings, net of tax, was $5,041 and $952, respectively. (4) Policy loans were reclassified from invested assets to insurance contract liabilities under IFRS 17 with no remeasurement and no impact to equity. (5) Own use real estate properties which are underlying items for insurance contracts with direct participating features were remeasured to fair value as if they were investment properties, as permitted by IFRS 17. This remeasurement resulted in an increase of carrying value of $1,035. The impact to retained earnings, net of tax, was $915. The Company has elected to apply the impairment requirements of IAS 39 (incurred losses) for the comparative period as provided for under IFRS 17. Accordingly, for assets that were classified as FVTPL under IAS 39, where no impairment was required, but were reclassified to FVOCI or amortized cost under IFRS 9 for the comparative period, the Company did not measure any impairment for the comparative period since IAS 39 impairment was not calculated. 157

2022 Annual Report Page 158 Page 160

2022 Annual Report Page 158 Page 160