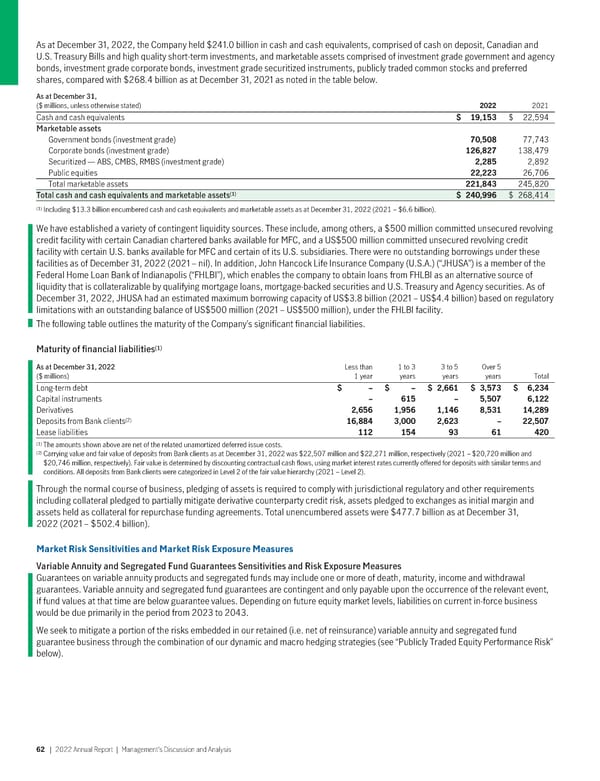

As at December 31, 2022, the Company held $241.0 billion in cash and cash equivalents, comprised of cash on deposit, Canadian and U.S. Treasury Bills and high quality short-term investments, and marketable assets comprised of investment grade government and agency bonds, investment grade corporate bonds, investment grade securitized instruments, publicly traded common stocks and preferred shares, compared with $268.4 billion as at December 31, 2021 as noted in the table below. As at December 31, ($ millions, unless otherwise stated) 2022 2021 Cash and cash equivalents $ 19,153 $ 22,594 Marketable assets Government bonds (investment grade) 70,508 77,743 Corporate bonds (investment grade) 126,827 138,479 Securitized — ABS, CMBS, RMBS (investment grade) 2,285 2,892 Public equities 22,223 26,706 Total marketable assets 221,843 245,820 (1) Total cash and cash equivalents and marketable assets $ 240,996 $ 268,414 (1) Including $13.3 billion encumbered cash and cash equivalents and marketable assets as at December 31, 2022 (2021 – $6.6 billion). We have established a variety of contingent liquidity sources. These include, among others, a $500 million committed unsecured revolving credit facility with certain Canadian chartered banks available for MFC, and a US$500 million committed unsecured revolving credit facility with certain U.S. banks available for MFC and certain of its U.S. subsidiaries. There were no outstanding borrowings under these facilities as of December 31, 2022 (2021 – nil). In addition, John Hancock Life Insurance Company (U.S.A.) (“JHUSA”) is a member of the Federal Home Loan Bank of Indianapolis (“FHLBI”), which enables the company to obtain loans from FHLBI as an alternative source of liquidity that is collateralizable by qualifying mortgage loans, mortgage-backed securities and U.S. Treasury and Agency securities. As of December 31, 2022, JHUSA had an estimated maximum borrowing capacity of US$3.8 billion (2021 – US$4.4 billion) based on regulatory limitations with an outstanding balance of US$500 million (2021 – US$500 million), under the FHLBI facility. The following table outlines the maturity of the Company’s significant financial liabilities. (1) Maturity of financial liabilities As at December 31, 2022 Lessthan 1to3 3to5 Over5 ($ millions) 1 year years years years Total Long-term debt $ – $ – $ 2,661 $ 3,573 $ 6,234 Capital instruments – 615 – 5,507 6,122 Derivatives 2,656 1,956 1,146 8,531 14,289 (2) Deposits from Bank clients 16,884 3,000 2,623 – 22,507 Lease liabilities 112 154 93 61 420 (1) The amounts shown above are net of the related unamortized deferred issue costs. (2) Carrying value and fair value of deposits from Bank clients as at December 31, 2022 was $22,507 million and $22,271 million, respectively (2021 – $20,720 million and $20,746 million, respectively). Fair value is determined by discounting contractual cash flows, using market interest rates currently offered for deposits with similar terms and conditions. All deposits from Bank clients were categorized in Level 2 of the fair value hierarchy (2021 – Level 2). Through the normal course of business, pledging of assets is required to comply with jurisdictional regulatory and other requirements including collateral pledged to partially mitigate derivative counterparty credit risk, assets pledged to exchanges as initial margin and assets held as collateral for repurchase funding agreements. Total unencumbered assets were $477.7 billion as at December 31, 2022 (2021 – $502.4 billion). MarketRiskSensitivitiesandMarketRiskExposureMeasures Variable Annuity and Segregated Fund Guarantees Sensitivities and Risk Exposure Measures Guarantees on variable annuity products and segregated funds may include one or more of death, maturity, income and withdrawal guarantees. Variable annuity and segregated fund guarantees are contingent and only payable upon the occurrence of the relevant event, if fund values at that time are below guarantee values. Depending on future equity market levels, liabilities on current in-force business would be due primarily in the period from 2023 to 2043. We seek to mitigate a portion of the risks embedded in our retained (i.e. net of reinsurance) variable annuity and segregated fund guarantee business through the combination of our dynamic and macro hedging strategies (see “Publicly Traded Equity Performance Risk” below). 62 | 2022AnnualReport | Management’sDiscussionandAnalysis

2022 Annual Report Page 63 Page 65

2022 Annual Report Page 63 Page 65