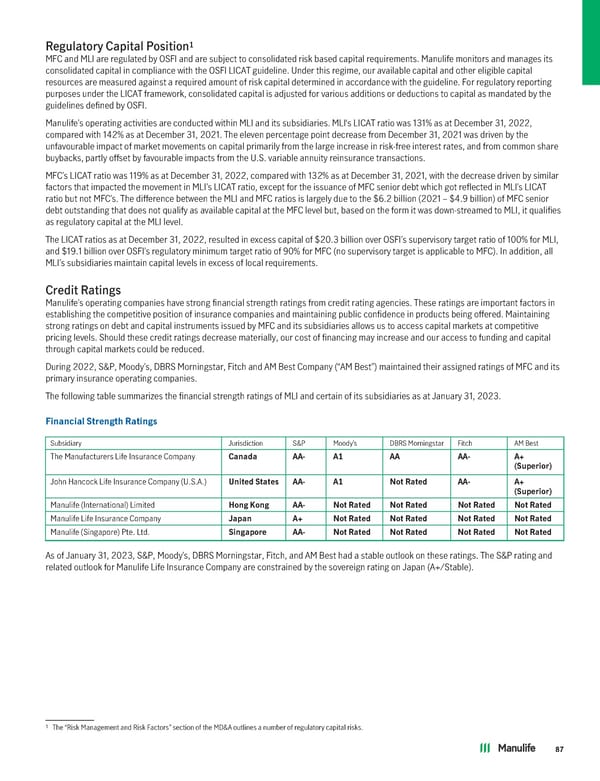

1 Regulatory Capital Position MFC and MLI are regulated by OSFI and are subject to consolidated risk based capital requirements. Manulife monitors and manages its consolidated capital in compliance with the OSFI LICAT guideline. Under this regime, our available capital and other eligible capital resources are measured against a required amount of risk capital determined in accordance with the guideline. For regulatory reporting purposes under the LICAT framework, consolidated capital is adjusted for various additions or deductions to capital as mandated by the guidelines defined by OSFI. Manulife’s operating activities are conducted within MLI and its subsidiaries. MLI‘s LICAT ratio was 131% as at December 31, 2022, compared with 142% as at December 31, 2021. The eleven percentage point decrease from December 31, 2021 was driven by the unfavourable impact of market movements on capital primarily from the large increase in risk-free interest rates, and from common share buybacks, partly offset by favourable impacts from the U.S. variable annuity reinsurance transactions. MFC’s LICAT ratio was 119% as at December 31, 2022, compared with 132% as at December 31, 2021, with the decrease driven by similar factors that impacted the movement in MLI’s LICAT ratio, except for the issuance of MFC senior debt which got reflected in MLI’s LICAT ratio but not MFC’s. The difference between the MLI and MFC ratios is largely due to the $6.2 billion (2021 – $4.9 billion) of MFC senior debt outstanding that does not qualify as available capital at the MFC level but, based on the form it was down-streamed to MLI, it qualifies as regulatory capital at the MLI level. The LICAT ratios as at December 31, 2022, resulted in excess capital of $20.3 billion over OSFI’s supervisory target ratio of 100% for MLI, and $19.1 billion over OSFI’s regulatory minimum target ratio of 90% for MFC (no supervisory target is applicable to MFC). In addition, all MLI’s subsidiaries maintain capital levels in excess of local requirements. Credit Ratings Manulife’s operating companies have strong financial strength ratings from credit rating agencies. These ratings are important factors in establishing the competitive position of insurance companies and maintaining public confidence in products being offered. Maintaining strong ratings on debt and capital instruments issued by MFC and its subsidiaries allows us to access capital markets at competitive pricing levels. Should these credit ratings decrease materially, our cost of financing may increase and our access to funding and capital through capital markets could be reduced. During 2022, S&P, Moody’s, DBRS Morningstar, Fitch and AM Best Company (“AM Best”) maintained their assigned ratings of MFC and its primary insurance operating companies. The following table summarizes the financial strength ratings of MLI and certain of its subsidiaries as at January 31, 2023. FinancialStrengthRatings Subsidiary Jurisdiction S&P Moody’s DBRS Morningstar Fitch AM Best The Manufacturers Life Insurance Company Canada AA- A1 AA AA- A+ (Superior) John Hancock Life Insurance Company (U.S.A.) UnitedStates AA- A1 NotRated AA- A+ (Superior) Manulife (International) Limited HongKong AA- NotRated NotRated NotRated NotRated Manulife Life Insurance Company Japan A+ NotRated NotRated NotRated NotRated Manulife (Singapore) Pte. Ltd. Singapore AA- NotRated NotRated NotRated NotRated As of January 31, 2023, S&P, Moody’s, DBRS Morningstar, Fitch, and AM Best had a stable outlook on these ratings. The S&P rating and related outlook for Manulife Life Insurance Company are constrained by the sovereign rating on Japan (A+/Stable). 1 The “Risk Management and Risk Factors” section of the MD&A outlines a number of regulatory capital risks. 87

2022 Annual Report Page 88 Page 90

2022 Annual Report Page 88 Page 90