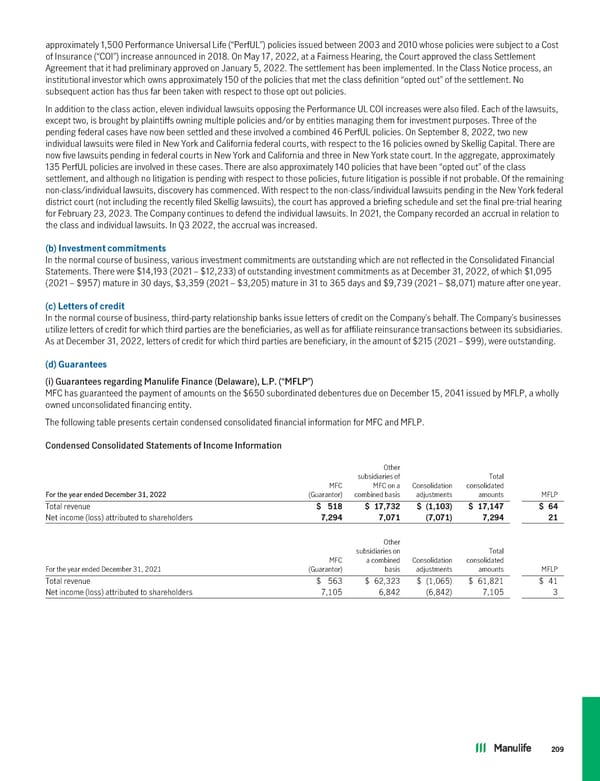

approximately 1,500 Performance Universal Life (“PerfUL”) policies issued between 2003 and 2010 whose policies were subject to a Cost of Insurance (“COI”) increase announced in 2018. On May 17, 2022, at a Fairness Hearing, the Court approved the class Settlement Agreement that it had preliminary approved on January 5, 2022. The settlement has been implemented. In the Class Notice process, an institutional investor which owns approximately 150 of the policies that met the class definition “opted out” of the settlement. No subsequent action has thus far been taken with respect to those opt out policies. In addition to the class action, eleven individual lawsuits opposing the Performance UL COI increases were also filed. Each of the lawsuits, except two, is brought by plaintiffs owning multiple policies and/or by entities managing them for investment purposes. Three of the pending federal cases have now been settled and these involved a combined 46 PerfUL policies. On September 8, 2022, two new individual lawsuits were filed in New York and California federal courts, with respect to the 16 policies owned by Skellig Capital. There are now five lawsuits pending in federal courts in New York and California and three in New York state court. In the aggregate, approximately 135 PerfUL policies are involved in these cases. There are also approximately 140 policies that have been “opted out” of the class settlement, and although no litigation is pending with respect to those policies, future litigation is possible if not probable. Of the remaining non-class/individual lawsuits, discovery has commenced. With respect to the non-class/individual lawsuits pending in the New York federal district court (not including the recently filed Skellig lawsuits), the court has approved a briefing schedule and set the final pre-trial hearing for February 23, 2023. The Company continues to defend the individual lawsuits. In 2021, the Company recorded an accrual in relation to the class and individual lawsuits. In Q3 2022, the accrual was increased. (b) Investmentcommitments In the normal course of business, various investment commitments are outstanding which are not reflected in the Consolidated Financial Statements. There were $14,193 (2021 – $12,233) of outstanding investment commitments as at December 31, 2022, of which $1,095 (2021 – $957) mature in 30 days, $3,359 (2021 – $3,205) mature in 31 to 365 days and $9,739 (2021 – $8,071) mature after one year. (c) Letters of credit In the normal course of business, third-party relationship banks issue letters of credit on the Company’s behalf. The Company’s businesses utilize letters of credit for which third parties are the beneficiaries, as well as for affiliate reinsurance transactions between its subsidiaries. As at December 31, 2022, letters of credit for which third parties are beneficiary, in the amount of $215 (2021 – $99), were outstanding. (d) Guarantees (i) Guarantees regarding Manulife Finance (Delaware), L.P. (“MFLP”) MFC has guaranteed the payment of amounts on the $650 subordinated debentures due on December 15, 2041 issued by MFLP, a wholly owned unconsolidated financing entity. The following table presents certain condensed consolidated financial information for MFC and MFLP. Condensed Consolidated Statements of Income Information Other subsidiaries of Total MFC MFC on a Consolidation consolidated For the year ended December 31, 2022 (Guarantor) combined basis adjustments amounts MFLP Total revenue $ 518 $ 17,732 $ (1,103) $ 17,147 $ 64 Net income (loss) attributed to shareholders 7,294 7,071 (7,071) 7,294 21 Other subsidiaries on Total MFC a combined Consolidation consolidated For the year ended December 31, 2021 (Guarantor) basis adjustments amounts MFLP Total revenue $ 563 $ 62,323 $ (1,065) $ 61,821 $ 41 Net income (loss) attributed to shareholders 7,105 6,842 (6,842) 7,105 3 209

2022 Annual Report Page 210 Page 212

2022 Annual Report Page 210 Page 212