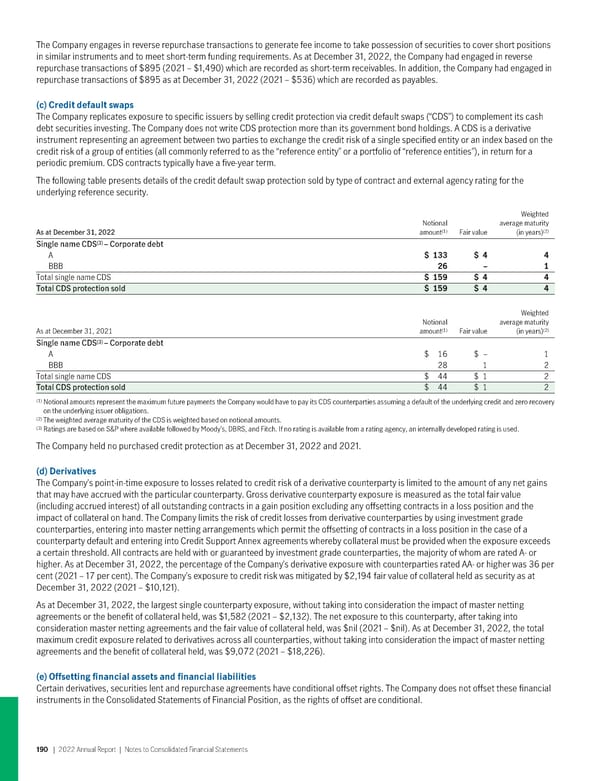

The Company engages in reverse repurchase transactions to generate fee income to take possession of securities to cover short positions in similar instruments and to meet short-term funding requirements. As at December 31, 2022, the Company had engaged in reverse repurchase transactions of $895 (2021 – $1,490) which are recorded as short-term receivables. In addition, the Company had engaged in repurchase transactions of $895 as at December 31, 2022 (2021 – $536) which are recorded as payables. (c) Credit defaultswaps The Company replicates exposure to specific issuers by selling credit protection via credit default swaps (“CDS”) to complement its cash debt securities investing. The Company does not write CDS protection more than its government bond holdings. A CDS is a derivative instrument representing an agreement between two parties to exchange the credit risk of a single specified entity or an index based on the credit risk of a group of entities (all commonly referred to as the “reference entity” or a portfolio of “reference entities”), in return for a periodic premium. CDS contracts typically have a five-year term. The following table presents details of the credit default swap protection sold by type of contract and external agency rating for the underlying reference security. Weighted Notional average maturity (1) (2) As at December 31, 2022 amount Fair value (in years) (3) Single name CDS – Corporate debt A $ 133 $ 4 4 BBB 26 – 1 Total single name CDS $ 159 $ 4 4 Total CDS protection sold $ 159 $ 4 4 Weighted Notional average maturity (1) (2) As at December 31, 2021 amount Fair value (in years) (3) Single name CDS – Corporate debt A $16 $ – 1 BBB 28 1 2 Total single name CDS $44 $ 1 2 Total CDS protection sold $44 $ 1 2 (1) Notional amounts represent the maximum future payments the Company would have to pay its CDS counterparties assuming a default of the underlying credit and zero recovery on the underlying issuer obligations. (2) The weighted average maturity of the CDS is weighted based on notional amounts. (3) Ratings are based on S&P where available followed by Moody’s, DBRS, and Fitch. If no rating is available from a rating agency, an internally developed rating is used. The Company held no purchased credit protection as at December 31, 2022 and 2021. (d) Derivatives The Company’s point-in-time exposure to losses related to credit risk of a derivative counterparty is limited to the amount of any net gains that may have accrued with the particular counterparty. Gross derivative counterparty exposure is measured as the total fair value (including accrued interest) of all outstanding contracts in a gain position excluding any offsetting contracts in a loss position and the impact of collateral on hand. The Company limits the risk of credit losses from derivative counterparties by using investment grade counterparties, entering into master netting arrangements which permit the offsetting of contracts in a loss position in the case of a counterparty default and entering into Credit Support Annex agreements whereby collateral must be provided when the exposure exceeds a certain threshold. All contracts are held with or guaranteed by investment grade counterparties, the majority of whom are rated A- or higher. As at December 31, 2022, the percentage of the Company’s derivative exposure with counterparties rated AA- or higher was 36 per cent (2021 – 17 per cent). The Company’s exposure to credit risk was mitigated by $2,194 fair value of collateral held as security as at December 31, 2022 (2021 – $10,121). As at December 31, 2022, the largest single counterparty exposure, without taking into consideration the impact of master netting agreements or the benefit of collateral held, was $1,582 (2021 – $2,132). The net exposure to this counterparty, after taking into consideration master netting agreements and the fair value of collateral held, was $nil (2021 – $nil). As at December 31, 2022, the total maximum credit exposure related to derivatives across all counterparties, without taking into consideration the impact of master netting agreements and the benefit of collateral held, was $9,072 (2021 – $18,226). (e) Offsetting financial assetsandfinancialliabilities Certain derivatives, securities lent and repurchase agreements have conditional offset rights. The Company does not offset these financial instruments in the Consolidated Statements of Financial Position, as the rights of offset are conditional. 190 | 2022AnnualReport | NotestoConsolidatedFinancialStatements

2022 Annual Report Page 191 Page 193

2022 Annual Report Page 191 Page 193