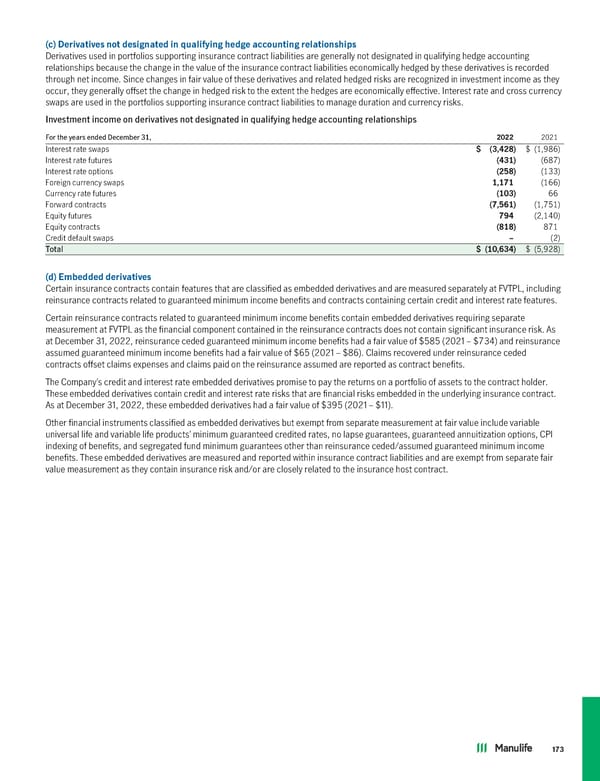

(c) Derivativesnotdesignatedinqualifyinghedgeaccountingrelationships Derivatives used in portfolios supporting insurance contract liabilities are generally not designated in qualifying hedge accounting relationships because the change in the value of the insurance contract liabilities economically hedged by these derivatives is recorded through net income. Since changes in fair value of these derivatives and related hedged risks are recognized in investment income as they occur, they generally offset the change in hedged risk to the extent the hedges are economically effective. Interest rate and cross currency swaps are used in the portfolios supporting insurance contract liabilities to manage duration and currency risks. Investment income on derivatives not designated in qualifying hedge accounting relationships For the years ended December 31, 2022 2021 Interest rate swaps $ (3,428) $ (1,986) Interest rate futures (431) (687) Interest rate options (258) (133) Foreign currency swaps 1,171 (166) Currency rate futures (103) 66 Forward contracts (7,561) (1,751) Equity futures 794 (2,140) Equity contracts (818) 871 Credit default swaps – (2) Total $ (10,634) $ (5,928) (d) Embeddedderivatives Certain insurance contracts contain features that are classified as embedded derivatives and are measured separately at FVTPL, including reinsurance contracts related to guaranteed minimum income benefits and contracts containing certain credit and interest rate features. Certain reinsurance contracts related to guaranteed minimum income benefits contain embedded derivatives requiring separate measurement at FVTPL as the financial component contained in the reinsurance contracts does not contain significant insurance risk. As at December 31, 2022, reinsurance ceded guaranteed minimum income benefits had a fair value of $585 (2021 – $734) and reinsurance assumed guaranteed minimum income benefits had a fair value of $65 (2021 – $86). Claims recovered under reinsurance ceded contracts offset claims expenses and claims paid on the reinsurance assumed are reported as contract benefits. The Company’s credit and interest rate embedded derivatives promise to pay the returns on a portfolio of assets to the contract holder. These embedded derivatives contain credit and interest rate risks that are financial risks embedded in the underlying insurance contract. As at December 31, 2022, these embedded derivatives had a fair value of $395 (2021 – $11). Other financial instruments classified as embedded derivatives but exempt from separate measurement at fair value include variable universal life and variable life products’ minimum guaranteed credited rates, no lapse guarantees, guaranteed annuitization options, CPI indexing of benefits, and segregated fund minimum guarantees other than reinsurance ceded/assumed guaranteed minimum income benefits. These embedded derivatives are measured and reported within insurance contract liabilities and are exempt from separate fair value measurement as they contain insurance risk and/or are closely related to the insurance host contract. 173

2022 Annual Report Page 174 Page 176

2022 Annual Report Page 174 Page 176