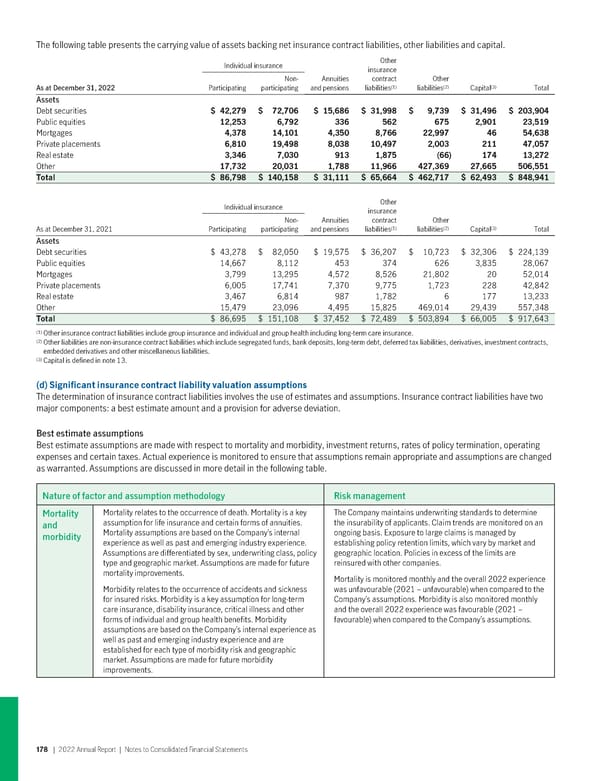

The following table presents the carrying value of assets backing net insurance contract liabilities, other liabilities and capital. Individual insurance Other insurance Non- Annuities contract Other (1) (2) (3) As at December 31, 2022 Participating participating and pensions liabilities liabilities Capital Total Assets Debt securities $ 42,279 $ 72,706 $ 15,686 $ 31,998 $ 9,739 $ 31,496 $ 203,904 Public equities 12,253 6,792 336 562 675 2,901 23,519 Mortgages 4,378 14,101 4,350 8,766 22,997 46 54,638 Private placements 6,810 19,498 8,038 10,497 2,003 211 47,057 Real estate 3,346 7,030 913 1,875 (66) 174 13,272 Other 17,732 20,031 1,788 11,966 427,369 27,665 506,551 Total $ 86,798 $ 140,158 $ 31,111 $ 65,664 $ 462,717 $ 62,493 $ 848,941 Individual insurance Other insurance Non- Annuities contract Other (1) (2) (3) As at December 31, 2021 Participating participating and pensions liabilities liabilities Capital Total Assets Debt securities $ 43,278 $ 82,050 $ 19,575 $ 36,207 $ 10,723 $ 32,306 $ 224,139 Public equities 14,667 8,112 453 374 626 3,835 28,067 Mortgages 3,799 13,295 4,572 8,526 21,802 20 52,014 Private placements 6,005 17,741 7,370 9,775 1,723 228 42,842 Real estate 3,467 6,814 987 1,782 6 177 13,233 Other 15,479 23,096 4,495 15,825 469,014 29,439 557,348 Total $ 86,695 $ 151,108 $ 37,452 $ 72,489 $ 503,894 $ 66,005 $ 917,643 (1) Other insurance contract liabilities include group insurance and individual and group health including long-term care insurance. (2) Other liabilities are non-insurance contract liabilities which include segregated funds, bank deposits, long-term debt, deferred tax liabilities, derivatives, investment contracts, embedded derivatives and other miscellaneous liabilities. (3) Capital is defined in note 13. (d) Significantinsurancecontractliabilityvaluationassumptions The determination of insurance contract liabilities involves the use of estimates and assumptions. Insurance contract liabilities have two major components: a best estimate amount and a provision for adverse deviation. Best estimate assumptions Best estimate assumptions are made with respect to mortality and morbidity, investment returns, rates of policy termination, operating expenses and certain taxes. Actual experience is monitored to ensure that assumptions remain appropriate and assumptions are changed as warranted. Assumptions are discussed in more detail in the following table. Nature of factor and assumption methodology Risk management Mortality Mortality relates to the occurrence of death. Mortality is a key The Company maintains underwriting standards to determine and assumption for life insurance and certain forms of annuities. the insurability of applicants. Claim trends are monitored on an morbidity Mortality assumptions are based on the Company’s internal ongoing basis. Exposure to large claims is managed by experience as well as past and emerging industry experience. establishing policy retention limits, which vary by market and Assumptions are differentiated by sex, underwriting class, policy geographic location. Policies in excess of the limits are type and geographic market. Assumptions are made for future reinsured with other companies. mortality improvements. Mortality is monitored monthly and the overall 2022 experience Morbidity relates to the occurrence of accidents and sickness was unfavourable (2021 – unfavourable) when compared to the for insured risks. Morbidity is a key assumption for long-term Company’s assumptions. Morbidity is also monitored monthly care insurance, disability insurance, critical illness and other and the overall 2022 experience was favourable (2021 – forms of individual and group health benefits. Morbidity favourable) when compared to the Company’s assumptions. assumptions are based on the Company’s internal experience as well as past and emerging industry experience and are established for each type of morbidity risk and geographic market. Assumptions are made for future morbidity improvements. 178 | 2022AnnualReport | NotestoConsolidatedFinancialStatements

2022 Annual Report Page 179 Page 181

2022 Annual Report Page 179 Page 181